As the U.S. staggers out of pandemic lockdown, investors could find values in its steps.

WEBINAR SUMMARY: OPPORTUNITIES IN A DISJOINTED RECOVERY

So far, so good for opportunity-minded investors.

Businesses in many U.S. states are cautiously unshuttering as the nation’s overall COVID-19 infection and fatality rates appear to be declining.

It is still early, but a feared resurgence of the highly contagious virus hasn’t yet appeared, and the economy is currently on track to be 80% reopened by the fall and fully operational by Dec. 31, according to AMG National Trust’s daily statistical modeling and analysis.

“For some of us who are really concerned about a second wave shutting us down again, this is very encouraging,” AMG Chairman Earl Wright said May 14th during an Insights briefing on the pandemic’s economic impact. Click here to watch the video.

If the deadly disease’s spread remains in decline or even on a plateau, investment opportunities could present themselves in coming months as the economy reboots and stock markets power up.

But for now, the economic news is grim. The U.S. unemployment rate stands at 14.7%, and the underemployment rate is 22.8%.

“Small businesses are absolutely getting annihilated,” Wright said, explaining that the bulk of layoffs are coming from owner-operator enterprises. Think local restaurants, hair salons and bowling alleys. They are part of the service sector, much of which closed down when governments ordered non-essential workers to stay at home in April to slow COVID-19’s spread.

That in turn tanked consumer spending, which accounts for about 70% of America’s GDP. Retail sales alone plummeted an estimated -16.4 % in April, after an -8.4% March dip. With consumers not buying products, manufacturing has also gone off a cliff.

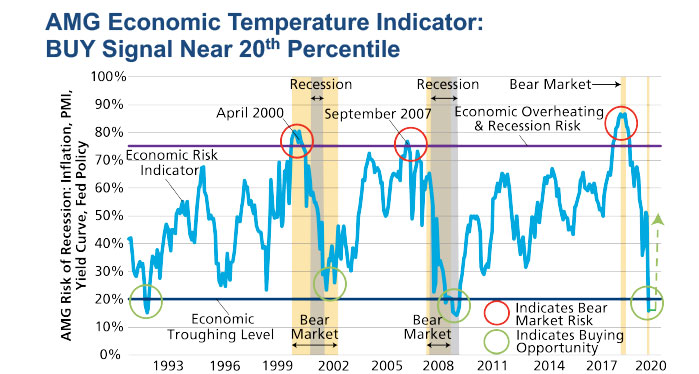

“Obviously, we are in a recession now,” said Josh Stevens, AMG’s Senior Vice President, Investment Group. First quarter GDP dropped an estimated -4.8% annualized; second quarter is expected to be far worse.

Opportunities are appearing as we near the bottom. But these will only be realized if the war against the deadly virus, which has killed more than 85,000 Americans, continues to successfully prevent a massive resurgence of infection.

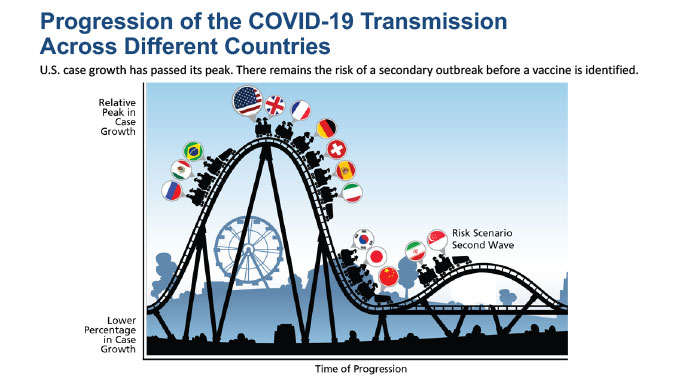

“It’s not a question of whether there will be a second wave. There will be,” Stevens said. It’s whether it will be a tidal wave forcing business to shut down again. Top U.S. public health officials this week warned lawmakers that reopening economies too quickly could lead to new outbreaks. Georgia, South Carolina and Texas failed to meet federal guidelines for reopening but did so anyway.

But so far, the news on the healthcare front is mostly positive.

- Europe, Asia and the United States are experiencing falling infection and fatality rates and are slowly reopening their economies. So far most of the world appears to be containing second waves of the viruses spread.

- In the United States, the disease isn’t spreading as fast as Americans don facemasks, socially distance themselves and frequently wash their hands. A statistical measurement shows the average number of people infected by someone with the disease is now somewhere between 1.0 and 1.1, down from 2.2 or higher. For comparison, someone with the flu infects an average of 1.4 other people. Anything below 1 means the rate of new cases and infectious spread of the disease is in decline.

- Worldwide, more than 200 treatments for COVID- 19 are in development, and 125 programs are searching for a vaccine with eight possibilities already in clinical trials.

- COVID-19 testing in the United States is accelerating rapidly with some 300,000 to 400,000 conducted daily, close to double what it was just a week ago. Experts expect 900,000 daily tests, if not more, will be needed as the country continues reopening and employees are frequently checked for infection.

As the U.S. economy’s resurrection takes hold in the second half of 2020, investors should be looking for opportunities on multiple fronts.

The S&P 500 has already recovered over 30% of its losses since the March 23 crash, and Nasdaq has regained nearly 50%. The market rebound has largely been pushed by six major companies, the near monopolistic FAANGM stocks: Facebook, Amazon, Apple, Netflix, Google (Alphabet), and Microsoft. Even though there has been significant recovery in these type holdings, there are opportunities in areas of the market that have not kept pace.

Economically cyclical stocks are equities that history indicates should have promising upsides in coming months. They have profits more tied to the economy. Catching them when the economy rebounds and markets begin a sustained climb could enhance returns as has happened in past recessions. These include small- and mid-cap, foreign and value stocks.

Looking at sectors, financial companies, which are 28% off their Feb. 19 peak, also could have a particularly rosy outlook. Community and regional banks have been particularly hit during the pandemic lockdown because they generally loan money to the small businesses and commercial real estate companies most affected. As restaurants and offices have closed, investors have grown concerned that these companies will no longer be able to repay their bank loans.

But easy-money policies and numerous government programs are flooding the market with liquidity, meaning banks are poised to perform well as the economy recovers, Stevens said. They can restructure loans, defer payments and work with stressed borrowers to better ensure against default.

“The banking industry, as far as their balance sheets go, is very, very strong,” Wright said, noting that financial reforms adopted after the 2008 financial crisis have helped ensure banks are adequately capitalized for this crisis.

In the long run, commercial real estate looks promising 12 to 18 months down the road.

This sector was generally healthy coming into 2020, but there were indications that values had peaked and the market was plateauing. Then the economic shutdown came and ignited a stress cycle.

“Tenant defaults and non-payment of rent are impairing property income,” said Dave Merritt, AMG Senior Vice President, Private Capital. “Discretionary brick-and-mortar retail, restaurant, hospitality and central-business-district office is being hit the hardest.

Vacancy and rent-collection issues will likely continue for the next year or so. Loan modifications and defaults will also probably keep accelerating. As this stress cycle wears on, pricing should drop at some point, and “attractive acquisition opportunities will be available,” Merritt said, noting that the recovery cycle could last for several years.

He explained that savvy investors should selectively choose property types and locations that add value. Investors should also be well capitalized and knowledgeable when it comes to operations because the competition will be fierce.

AMG thinks multi-family housing could be an attractive sector. New home construction was already in decline because of affordability issues when the pandemic hit. That trend likely will continue as unemployed workers return to jobs. There is a pent-up demand for affordable housing units, he said.

Industrial real estate could also prove favorable as the economy restarts and the rapid growth in online retailing begins again. Companies like Amazon increasingly need distribution centers that industrial real estate provides.