Inflation is waning, but it’s proving a sticky problem for the Federal Reserve (Fed), which seems determined to wipe it out—even if it means a recession, AMG Chairman Earl Wright told clients this month during an Insights seminar.

The U.S. central bank keeps hammering away at inflation with almost monthly interest rate hikes, including this week’s 0.25 percentage point increase in the Fed’s target range for the federal funds rate, which now stands at 4.75-5%. Last March, the range was 0.25-0.50%.

The inflation rate last month was at 6.04%, compared to 6.41% in January and 7.87% in February last year, according to the Consumer Price Index. Inflation peaked to a 40-year high last June at 9.1%. The Fed aims to bring it down to around 2%.

Rapid rate hikes are not tamping down the inflation fires as fast as we all would like, and it’s starting to have a profound impact on the overall economy, Wright said. He pointed to the recent spate of bank failures and the continuing bear stock market.

“The real question is how high rates will go,” he said. “5.25%, 5.5%? Some really sophisticated people say 6%. And how long will they stay there? That could be as impactful as raising rates themselves.”

AMG expects rates to continue rising into the second quarter, and not start dropping until sometime in 2024, causing the U.S. economy to experience a mild recession or severe slowdown in coming months. The longer rates stay high, the greater the chance of recession.

Dr. Michael Bergmann, AMG’s chief economist, anticipates the Fed will raise rates again in May and June to around 5.5%, and then call it quits.

“And it will stay there,” he said, “until (Fed policymakers) are quite confident that the economy has slowed, the employment markets have developed some slack, and most importantly, inflation is clearly coming down and going in the neighborhood of their 2% target.”

Wright stated that keeping rates high into 2024 will likely hurt the U.S. job market, where the unemployment rate stands now at 3.6%, slightly up from a 50-year low of 3.4% in January.

Currently, there are 5.9 million unemployed workers and 10.6 million unfilled jobs. The service sector, hardest hit by the pandemic, is still hiring people as fast as possible.

“People are out doing stuff … but there are too few workers,” Wright said, noting that employers are having to pay more to fill jobs and that wage growth is one reason inflation remains persistent.

Despite all the jobs available, Bergmann pointed out that wage growth is slowing, and unemployment is gradually increasing, which are reducing inflationary pressures. In addition, consumer spending is shifting from goods, which has been highly inflationary, to services, which are less so. And rental rates in newly signed housing leases are “falling like a rock.”

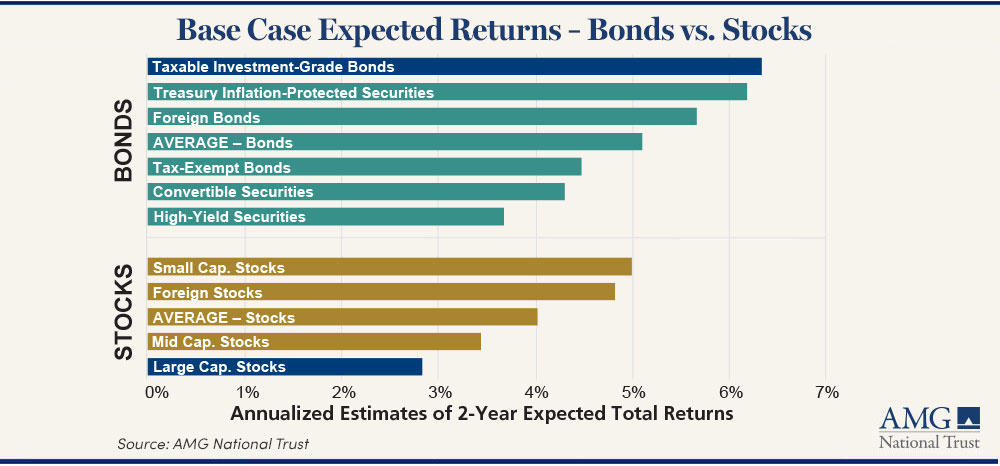

If there is a bright spot from higher interest rates, it’s in the bond markets. In general, Bergmann said, bond returns are expected to be better than stocks in the coming months, and taxable bonds will probably be twice as good as growth stocks.

HOW AMG CAN HELP

AMG is a trusted resource for many families, especially those with complicated financial lives. We’re here to help you build and manage your wealth. To find out more about AMG’s Personal Financial Management (PFM) or to book a free consultation call 303-486-1475 or email us the best day and time to reach you.