TAXING ISSUES: WHAT IT COULD MEAN FOR YOUR PORTFOLIO IF DEMOCRATS SWEEP TO POWER

Many investors are asking how a blue wave of November election victories might affect the U.S. economy, financial markets and their portfolios.

Democratic candidates are promising to raise taxes, particularly on the wealthy, to fund proposed government programs ranging from 12 weeks of paid family leave to rebuilding the nation’s infrastructure.

Will that mean increased market volatility? A stunted economy? Runaway inflation?

AMG National Trust addressed those questions in its August 13 webinar: Presidential Election and Policy Impact. Click here to watch the webinar.

If Democrats win the White House, capture a majority of U.S. Senate seats and maintain control of the House of Representatives, one thing is absolutely certain. The world won’t stop spinning.

But significant changes in federal government policies almost assuredly will follow.

“The economic impact long-term is not grave,” said AMG Chairman Earl Wright, “but it does have implications investors need to understand.”

Right now America continues to grapple with the COVID-19 pandemic and the recession it caused. Vaccine development looks promising, but the upcoming Nov. 3 general election only adds to uncertainty about America’s economy and direction. So investors are wise to discuss concerns with their financial counselors and plan for possible changes regardless of who wins.

Economic policy uncertainty is a concern everywhere. But it is higher here in the U.S. now than anywhere else in the world. That’s the opposite of the Great Recession a decade ago, when Europe and China – the world’s other economic behemoths – topped the uncertainty charts. U.S. politics and the upcoming election are key reasons for the reversal.

“When we go through a crisis period, the policy responses to that crisis have implications for the longer-term outperformance of financial assets,” said Josh Stevens, Senior Vice President – Investment Group. “And right now it’s a bit up in the air.”

Despite all that, the United States remains on track to return to pre-pandemic GDP levels in early 2022 with consumer spending resuming normal patterns later that year, according to AMG’s base-case economic scenario.

That long-term forecast probably won’t change too much because of the election, even if Democrats take control of all three branches of government, as recent polls suggest is highly possible.

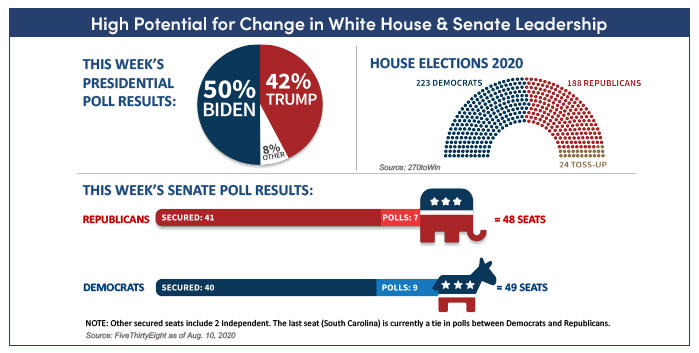

“If the election were held today, we would have a President Biden … the House would still be controlled by Democrats and Speaker Pelosi,” Wright said, noting that the Senate is much more in play. Democrats are poised to control either 48 or 49 of 100 seats, with two left-leaning independents (Bernie Sanders of Vermont and Angus King of Maine) essentially giving them a majority.

AMG expects that a Joe Biden presidency, based on his campaign proposals, would boost U.S. spending by more than $3.4 trillion from 2021 to 2030. That’s an 8.5% average annual increase ($378 billion) over the $4.45 trillion the federal government spent in fiscal year 2019.

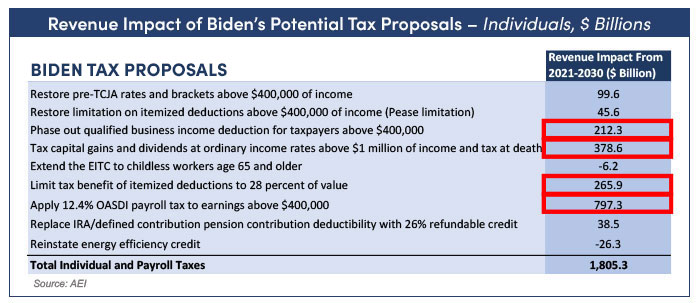

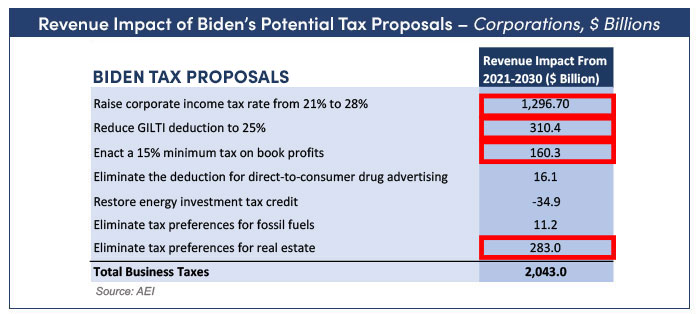

To pay for it, Biden and other Democrats have proposed raising both individual and corporate taxes. For individuals, taxpayers earning over $400,000 a year could potentially face significant increases in overall income taxes. Corporations probably would see their tax rates climbing from 21% to 28% among other changes. Estate laws also could change.

If all the potential income tax changes happen, the top 1% of earners in America could see their after-tax income in 2021-2029 decrease by nearly 18%, according to the American Enterprise Institute. That rate would fall to nearly 14% by 2030.

So what impact would these possible tax increases have on the overall economy?

“It’s not very significant,” Wright said, noting that GDP might fall by as much as 0.2% from 2021 through 2030. “It’s a big impact on the top 1% … but there’s nothing that says we’re going to be thrown into a depression. There’s nothing that says we’re going to be thrown into a recession. It just says that basically our economy and this recovery will be slowed down a bit.”

Long-term, however, companies won’t reinvest their capital as much or see the productivity gains they might see under different tax policies, Wright said. But nothing catastrophic is likely to happen.

The same holds true for financial markets.

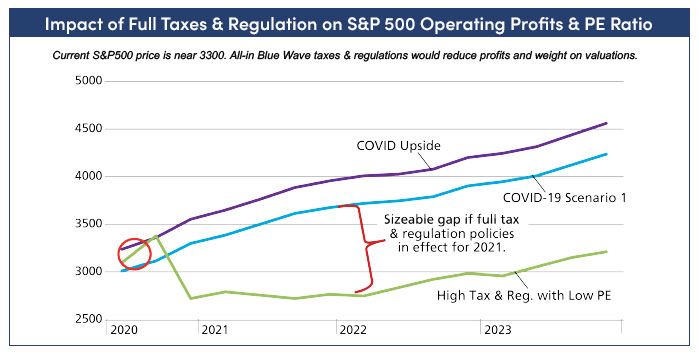

AMG’s Stevens said the proposed tax policies would likely have a negative effect on corporate profits, causing them to possibly fall by up to 15%. Stock valuations (PE ratio) would also be modestly lowered. But on a positive, low interest rates and bond yields would help support stock prices. U.S. stock returns would be substantially lower, but that’s in part because they have been historically high.

“Instead of the 9 to 10% (average) returns we saw over the past 100 years or so,” he said, “we might be seeing 5 to 6% over the next decade.”

Stock are still likely to outperform bonds, Stevens continued, but warned that a market correction is possible as investors think about the ramifications of higher tax rates on corporate profits.

Raising taxes and higher government spending, along with other potential Democratic policies such as increased regulation, might also have a negative impact on the U.S. dollar, which raises the specter of higher inflation.

“Not next year,” Stevens said, “but three or four years down the road.”

Bottom Line

AMG believes investors should consider two paths going forward, depending on their tax situation and risk tolerance:

Short-term risk averse – If you are concerned about the next three to four months, trim U.S. stock holdings and keep short-term bonds. The downside is that it’s sometimes tough to get back into the markets.

Long-term risk averse – Cut domestic equities and reallocate to asset classes like foreign stocks, hedge funds and private capital with higher long-term return potential. Diversify holdings into asset classes such as precious metals, currencies and real estate. The downside is that long-term winners might lose money in the short run.

Taxes – Because capital-gains taxes might go up, ponder taking long-term gains this year and losses in following years.