• 7 min read

Sign up to receive an email summary of new articles posted to AMG Research & Insights.

New presidential administrations bring with them new and recalibrated policies. Investors need to understand these policy changes through an economic lens, particularly how policy may be implemented and the subsequent impact on managing your wealth.

As the first event of its 50th anniversary year, AMG held a webinar to release its 2025-2027 Economic Outlook with insight from Chairman Earl Wright; Dr. Michael Bergmann, Chief Investment Officer; Dr. Jarek Strzalkowski, Global Macro Economist; Josh Stevens, Senior Vice President, AMG Capital Management; and Chris Jacoby, Senior Vice President, Private Capital.

Potential economic scenarios were discussed. A “Soft Landing” is AMG’s base case, or most likely scenario, and anticipates that tax cuts are extended, tariffs are limited, and the U.S. economy experiences a mild slowdown in 2025 but recovers later in the year.

A more positive scenario, “No Landing, but Higher Productivity,” anticipates significant regulatory reform leading to productivity gains and stronger economic growth. On the other hand, a third scenario, “Trade Wars,” explores the negative impacts of heavy tariffs being met with retaliation and a global trade war.

Heading into 2025, the economy appears in fairly good shape, Dr. Strzalkowski said.

Over the past seven quarters, the economy grew, on average, by almost 3% a year—faster than the pre-pandemic average of 2.4%. U.S. consumer spending accounted for over 70% of those gains. The labor market also revved up the economy, despite some signs of softening beyond pre-pandemic levels.

The direction from here depends on many factors, including policies coming from Washington.

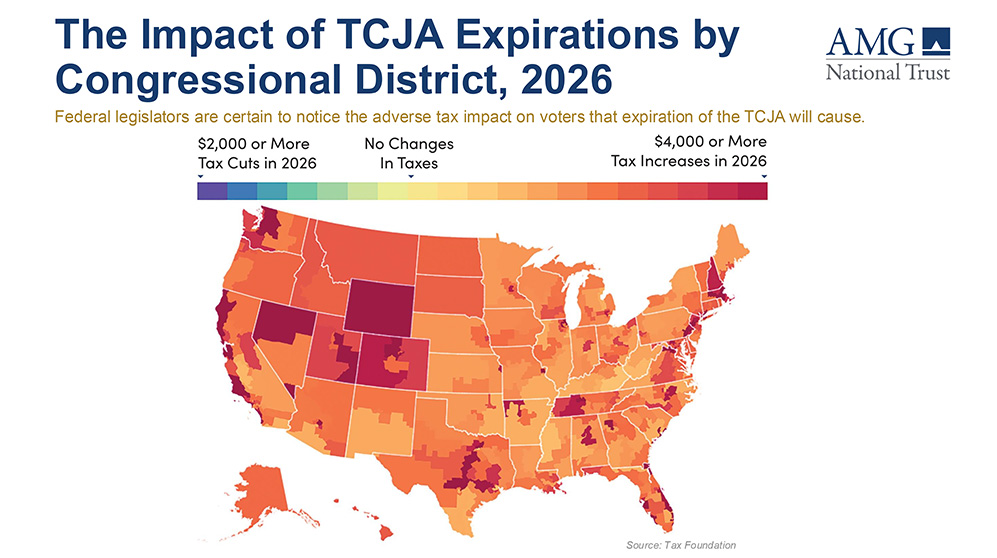

Several key portions of the Tax Cuts and Jobs Act (TCJA), such as lower individual tax rates, are scheduled to sunset on December 31, 2025. However, Dr. Bergmann said there’s little chance of that happening, particularly because expiration would have a negative impact on consumers, and “consumers are the backbone of what we’ve seen in terms of growth.”

Rather than expecting a large wave of deportations, AMG’s base case assumes targeted deportations primarily focused on individuals with criminal backgrounds or who have been denied asylum.

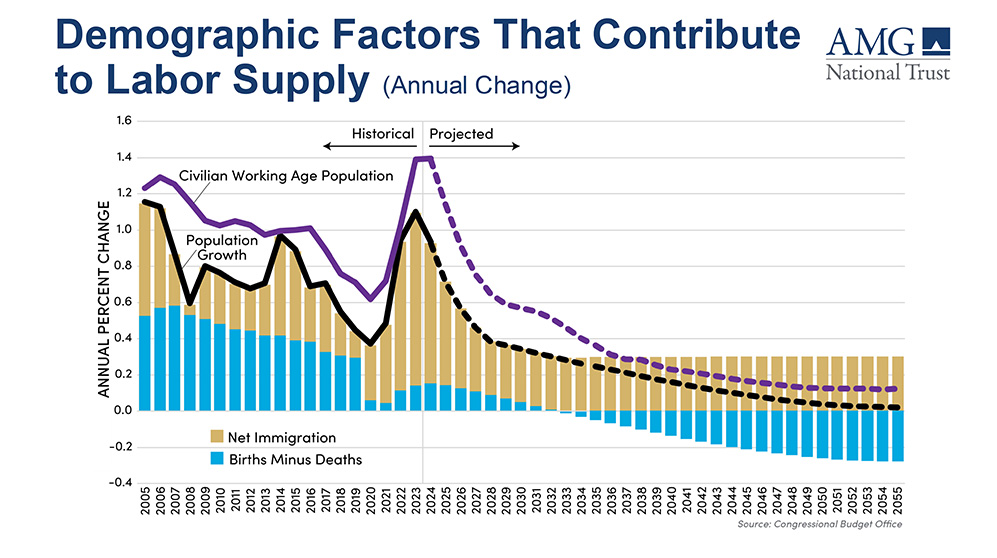

Why does AMG hold this view? Immigration is essential to U.S. economic growth.

Congressional Budget Office projections show that the number of deaths in the United States is going to surpass the number of births in the early 2030s. Without immigration, the U.S. population—and the labor force—will begin to decline, and “that would obviously be bad news for the U.S. economy.”

Another factor is that deportation carries an excessive cost, with different estimates conducted by various organizations over the past 15 years (adjusted to 2024 dollars) ranging from $12,000 per individual to more than $60,000.

Regulations are issued by federal agencies to implement the laws passed by Congress. In 2023 alone, more than 3,000 federal regulations were issued, taking up 85,000 pages in the Federal Register.

The total regulatory cost in 2023 was about $3.1 trillion (11% of GDP), according to a survey by the National Association of Manufacturers. To have a positive impact on the economy, Dr. Bergmann said, “We don’t even have to cut stuff. We just slow down the rate of new regulations. (By doing so) we could get a substantial boost to GDP and GDP growth.”

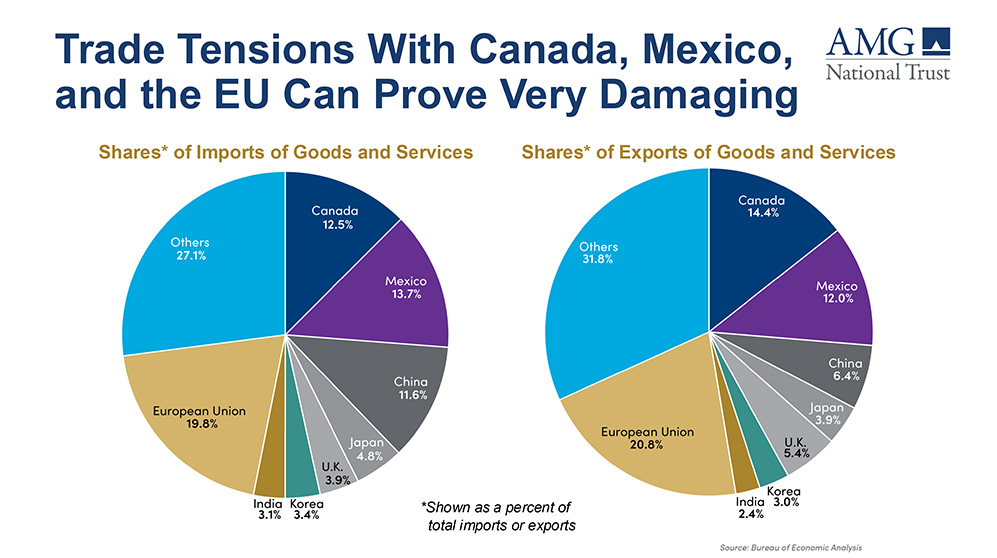

AMG tends to view the threat of tariffs as possibly more of a negotiating tactic. For example, proposed 25% tariffs on Canada and Mexico are a “truly horrible idea” because they currently are the two largest U.S. trading partners, Dr. Strzalkowski said, particularly in the automotive sector with closely integrated supply chains. Tariffs against one nation would potentially ricochet against the others.

The “Soft Landing” scenario assumes a 30% tariff on China and a slight increase in tariffs on other trade partners. While these moves would impose some additional costs on U.S. consumers, it’s not something that could wreck the U.S. economy, he said.

However, the “Trade War” scenario assumes a much higher tariff on China—60%—and a 10% blanket tariff on the rest of the world. That would bring average tariffs imposed by the United States to levels last seen in the 1930s and could cause a severe disruption in international trade.

AMG expects a broadening out of stock market of performance from the Magnificent 7 (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla) that should support small- and mid-cap stocks as well as the other 493 companies within the S&P 500. This does not mean sell the Magnificent 7 or the size-weighted S&P 500, just that other areas of the stock market should do well too. Additionally, Mr. Stevens emphasized we do not expect a recession and end to the bull market, but market appreciation is likely to slow from its torrid pace of the last two years.

In that context, the base case anticipates a slowdown in consumer spending and a re-acceleration in other sectors within the economy that supports relative performance in small- and mid-cap stocks and elsewhere.

Current opportunities in alternative investments also can help diversify portfolios. In focusing the discussion on venture capital, real estate, and energy, Mr. Jacoby said the impact of these investments’ is viewed both through a two- to three-year window for in-place/existing investments and in longer durations of 10-plus years for new investments.

A changing regulatory environment could allow for an uptick in liquidity and help propel artificial intelligence (AI) and the wave of innovation around it.

Consider biotech, where AI is being applied to research on proteins that are essential for many biological processes and the pipeline of innovative drugs. AI is also having an impact on financial services, logistics, and software development.

Several data points suggest a 12- to 24-month window of opportunity for investing in commercial real estate, Mr. Jacoby said.

First, valuations remain attractive for acquisitions now before real estate prices begin to appreciate.

Second, construction activity is slowing. At the same time, there is a housing unit shortage of three to five million units.

Mr. Jacoby said this is likely to lead to persistent demand for rental housing that would serve to lower the vacancy rates and allow for sustained rent growth.

The new administration has reiterated its mantra of drill, baby, drill and declared a national energy emergency. AMG expects the federal government to streamline the permitting process; open access to federal lands; and expand exports, primarily through permitting of liquified natural gas facilities.

In the wake of the long period of zero interest rates, which reduced opportunities, investors would be likely to “actually make money now by investing in fixed income,” Dr. Bergmann said in discussing investment returns

The outlook is also positive among equities.

For investors considering putting more in bonds, Dr. Bergmann cautioned them to also consider the tax impact. Gains in equities are taxed at the capital gains rate while income from bonds is taxed at the higher ordinary income rate.

The takeaway, he said, is that “you need a well-diversified portfolio.”

Not a client? Find out more about AMG’s Personal Financial Management (PFM) or to book a free consultation call 303-486-1475 or email us the best day and time to reach you.

This information is for general information use only. It is not tailored to any specific situation, is not intended to be investment, tax, financial, legal, or other advice and should not be relied on as such. AMG’s opinions are subject to change without notice, and this report may not be updated to reflect changes in opinion. Forecasts, estimates, and certain other information contained herein are based on proprietary research and should not be considered investment advice or a recommendation to buy, sell or hold any particular security, strategy, or investment product.