Though its beginnings reach back more than a decade, Bitcoin became a household name in 2017 when its value skyrocketed more than 1,300% over the course of the year. The prices of Bitcoin and many other so-called “cryptocurrencies” have since fallen by more than four-fifths from those early-2018 peaks,1& but investors, corporations, and regulators around the world have begun to take a serious look at the growing digital currency industry and the technology that underpins it: blockchain.

WHAT IS BLOCKCHAIN?

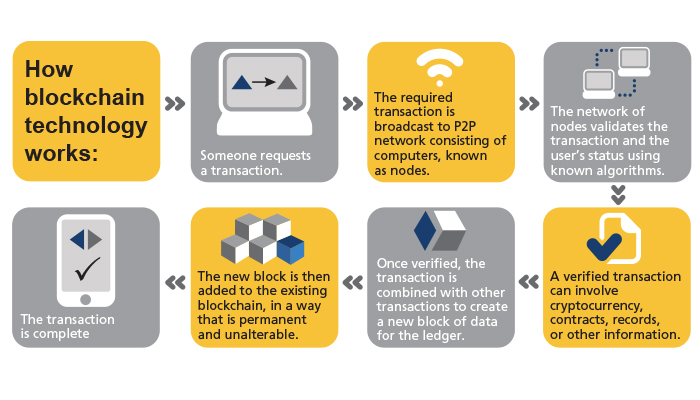

The modern concept for blockchain was presented in a 2008 white paper entitled “Bitcoin: A Peer-to-Peer Electronic Cash System,” authored by a person or group using the now-infamous pseudonym Satoshi Nakamoto. The paper outlines a vision for a decentralized payment network in which various types of transactions are validated by other peers on the network using computer encryption algorithms. These validated transactions are then combined into “blocks” of data and added to the existing collection of blocks, known as the blockchain.

The order and contents of the blockchain are known to all users connected to the network, meaning no central bank or authority is in charge of maintaining the historical ledger of transactions. To prevent fraud, transactions are validated and blocks are placed by users known as miners. Miners are computers on the network that ensure transactions are legitimate and then solve cryptographic “proof-of-work” problems before adding new blocks of transactions to the blockchain. These proof of work problems ensure that it is computationally unfeasible for any user to ever go back and make changes to the historical blockchain.

CURRENT ENVIRONMENT FOR BLOCKCHAIN

The decentralization, immutability, and transparency of blockchain make it an attractive tool for use in many areas of the global economy. In fact, corporations and governments around the world are already beginning to explore new applications for blockchain. Some of the current uses of blockchain technology include:

- Trade: Companies are using blockchain technology to track the progress of global shipments, to manage supply chains, and even to help consumers connect the ingredients in the foods they eat or the products they buy to their respective sources. One example is IBM Blockchain, which helps companies manage their supply chains top-to-bottom in real time.

- Finance: Blockchain-based asset exchanges are appearing in many forms, from services that allow users to trade various cryptocurrencies to services that help settle trades on actual stock exchanges. Stock exchanges in the U.S., Japan, Germany, Australia, India, and elsewhere are already exploring ways in which blockchain can expedite the settlement of trades and reduce fees. Major insurers, like Nationwide, have begun using blockchain technology to provide instant proof-of-insurance to policyholders. Also, blockchain startups, like Circle, are aiming to create faster and cheaper global payment networks with blockchain technology.

- Healthcare: Various healthcare-oriented blockchain startups have appeared that use blockchain to securely maintain patient medical records and share them with desired providers. Other companies, such as Nano Vision, are using blockchain healthcare data and artificial intelligence to identify patterns of disease that could lead to new medical breakthroughs.

- Entertainment: The transparency of blockchain is ideal for tracking how many people use an artist’s content, and companies, like Spotify, are exploring how blockchain can be used to make sure artists get paid fairly. Blockchain is also being used to create cross-platform videogames, to eliminate concert ticket fraud, and to help event organizers share and control costs.

- Smart Contracts: Transcending many industries, blockchain-based smart contracts are already being used in everything from real estate agreements to peer-to-peer lending to airline flight insurance. Smart contracts remove the need for middlemen in many cases, which makes the creation and execution of contracts faster and less expensive. One startup, Etherparty, has even created a tool that allows users to choose from a variety of blockchain smart contract templates based on their particular needs.

OUTLOOK FOR BLOCKCHAIN

The applications for blockchain continue to grow, and the technology has begun gaining favor in some of the most important areas of trade and finance. In June 2018, for example, the central bank of South Africa confirmed that it had successfully tested a blockchain-based system for clearance and settlement between its member banks.2 Also, groups like the Wall Street Blockchain Alliance—comprised of over 270 organizations from areas such as trade, finance, and law—are partnering with organizations like the Association of International Certified Professional Accountants and the Blockchain in Transport Alliance to help integrate blockchain with the modern economy.3

While major institutions and corporations are beginning to explore blockchain, there are also a variety of new startups that specialize in blockchain technology. Through just the first three quarters of 2018, the number of venture capital deals funding blockchain-oriented companies was already double that of 2017, and the total amount of money funded was nearly four times greater.4 Many of these new companies plan to act as blockchain service providers or consultants, helping other organizations integrate blockchain into their operations. Expect organizations in industries like shipping, real estate, entertainment, law, insurance, healthcare, and financial services, plus governments and non-profits, to continue adopting blockchain technology in the coming years.

For the moment, however, blockchain is probably best-known for the role it plays in the creation and maintenance of cryptocurrencies like Bitcoin.

WHAT IS CRYPTOCURRENCY?

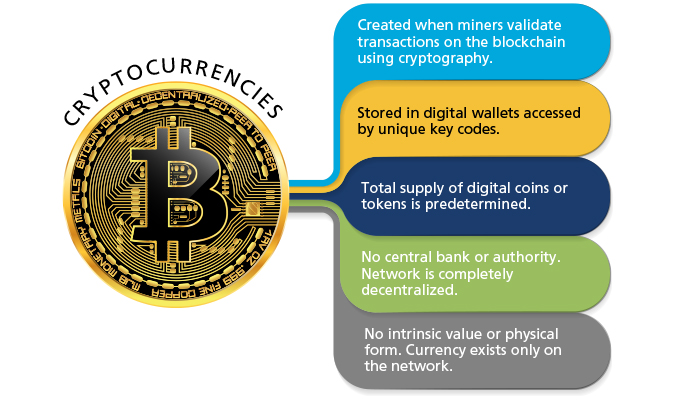

It takes time, energy, and computing power for miners on a blockchain network to validate transactions, create new blocks, and maintain a blockchain. As compensation, miners are awarded with a pre-specified amount of digital currency—cryptocurrency—each time they use cryptography to complete a new block and add it to the blockchain. In the case of the Bitcoin blockchain network, the digital currency created and paid to the miners is, naturally, Bitcoin.

Other blockchain networks have their own digital currencies, and it is important to note that not all cryptocurrencies are created in the same way Bitcoin is. Many other blockchain networks have unique designs and sets of rules. The key similarity between most cryptocurrencies, however, is that they are digital currencies that store and transmit value using a blockchain.

In the case of Bitcoin, once miners receive their digital currency, they can store and send it to others using the Bitcoin blockchain network. Cryptocurrencies are typically stored in digital “wallets” secured by a pair of unique public and private keys. Public keys can be shared like addresses to receive funds or send funds to others, but both the public and private keys are required to access any funds stored in a wallet.

Being built on blockchain technology, conventional cryptocurrencies have no oversight by central banking authorities. Most also have a fixed, pre-determined supply of digital “coins” that, once mined, cannot be reabsorbed or increased. These attributes could make some cryptocurrencies an attractive store of value for investors, similar to gold or other precious metals. Further, even though cryptocurrencies exist only on their respective networks and have no intrinsic value or physical form of their own, the real-world use cases for cryptocurrency continue to increase.

CURRENT ENVIRONMENT FOR CRYPTOCURRENCY

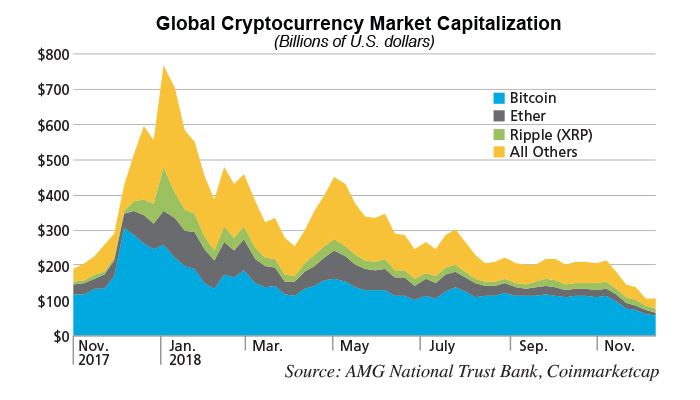

Cryptocurrencies exploded onto the public stage in 2017, when the total market capitalization—or market value—of cryptocurrencies worldwide rose from about $18 billion to almost $570 billion over the course of the year.5 Much of the increase in value was driven by speculation, as well as the desire of people in countries with volatile or weakening currencies to convert to other currencies.

In early 2018, regulators around the world began to clamp down on cryptocurrency transactions, particularly in the high-demand markets of China, Japan, and South Korea. Cryptocurrency prices plummeted as a result, and today remain far below their early-2018 highs. Nevertheless, investors and regulators alike have taken note of the significant potential value of cryptocurrencies.

As of November 2018, the three largest cryptocurrencies by market capitalization were Bitcoin, Ethereum network’s currency Ether, and Ripple network’s currency XRP. Unlike the Bitcoin blockchain, which only allows Bitcoin transactions, Ethereum strives to be a generic blockchain platform on which many different cryptocurrencies can operate. Many of the new cryptocurrencies that have appeared in recent years have been built on the Ethereum platform. Ripple, generally viewed as more amenable to the traditional corporate sector, aims to become a global payment network that connects banks, payment providers, asset exchanges, and corporations around the world.

Despite the decline in cryptocurrency values in 2018 and increased regulatory scrutiny, there are now over 2,000 active cryptocurrencies that have been issued by governments, corporations, and individuals worldwide.6 While many of these currencies are unlikely to be used or retain their value, and some may be outright fraudulent, other cryptocurrencies are developing real-world use cases. Some of the ways in which cryptocurrencies are now seen or used in everyday life include:

- ATMs: As of November 2018, there were nearly 4,000 cryptocurrency ATMs worldwide, spanning 74 different countries.7 Unlike conventional ATMs, which allow users to access their bank accounts, these machines—found at gas stations, sports bars, and other storefronts—allow users to quickly buy, sell, and/or trade cryptocurrencies with cash and a cryptocurrency wallet address.

- Payments & Purchases: Ripple is just one example of a company using cryptocurrency to maintain a fast, cheap, global payment network. Familiar small-business payment service provider Square has been approved for a patent that will allow any merchants using its service to accept payments in cryptocurrencies and have them automatically converted to the currency of their choice.8 Cryptocurrency is also used to move money internationally and to avoid the various obstacles and fees associated with international transactions.

- Governments: In an effort to recover from economic collapse and a steep decline in its local currency, the Venezuelan government recently issued its own cryptocurrency called the Petro coin. The value of the Petro is supposedly tied to the value of Venezuela’s vast oil reserves. While the coin has not been used as actual currency to date, Venezuela recently issued a new sovereign currency that is linked to the value of the Petro.

- Charitable Donations: The transparency of cryptocurrencies allows charitable givers to track their money from the time of donation all the way to its end use, a desirable trait for many who donate to charity. Cryptocurrencies, like Donationcoin and AidCoin have been created to serve this purpose.

- Asset Trading: There are now a variety of online cryptocurrency exchanges that allow users to transfer and convert among cryptocurrencies, as well as a few, like Gemini Exchange, that permit users to convert to or from fiat currencies like the U.S. dollar. The Chicago Board Options Exchange and Chicago Mercantile Exchange have also unveiled tradable futures contracts tied to the price of Bitcoin. Other large institutions have also begun to enter the space: Fidelity Investments recently announced it would trade and take custody of cryptocurrencies for its clients, and the owner of the New York Stock Exchange has announced plans to open its own Bitcoin exchange.

While cryptocurrencies have been particularly popular in economically unstable countries with weakening currencies in recent years—such as Venezuela, South Africa, Turkey, and Uganda—there are many attributes of cryptocurrencies that appeal to all investors. These characteristics include fraud and counterfeit prevention, a fixed money supply, no dependence on a central monetary authority, irreversible and pseudonymous transactions, and the potential for faster and cheaper transactions in some cases. Startups have also flocked to cryptocurrencies as a means of raising money through initial coin offerings (ICOs).

REGULATION OF CRYPTOCURRENCIES

In terms of regulation, positions on cryptocurrencies vary widely by country. Japan, home to one of the world’s largest cryptocurrency markets, has classified Bitcoin and other cryptocurrencies as fully taxable legal tender, and requires any cryptocurrency exchanges operating in the country to register with government regulators.9 South Korea does not yet tax gains from cryptocurrency investments, though any exchanges operating in the country must be registered and are closely monitored by regulators. China has completely banned financial institutions from handling Bitcoin transactions and does not allow either cryptocurrency exchanges or ICOs.

In Europe, member nations of the European Union (EU) are barred from releasing their own cryptocurrencies, and cryptocurrency-fiat exchanges are regulated under the EU’s anti-money laundering laws. Certain members of the EU—namely Germany, France, and Italy—also require cryptocurrency exchanges to register with their respective national regulators. Taxation of cryptocurrencies in Europe varies by country.10

In the United States, cryptocurrencies remain in something of a regulatory limbo. The Securities and Exchange Commission (SEC) has stated that it is likely to consider most cryptocurrencies financial securities, meaning the vast majority of ICOs in the United States in recent years were not registered or documented properly. The SEC has begun to levy fines and penalties in some of these cases.11 The Internal Revenue Service currently treats cryptocurrency as taxable property or income. The Financial Crimes Enforcement Network does not consider cryptocurrencies to be legal tender, but does classify cryptocurrency exchanges as money transmitters subject to its jurisdiction. The Commodities Futures Trading Commission views Bitcoin as a commodity and allows financial derivatives based on Bitcoin to trade publicly. U.S. lawmakers are currently working with the Justice Department to form a more cohesive strategy on how to regulate cryptocurrencies and digital asset exchanges.

As financial watchdogs in the United States and around the world grapple with how best to monitor the use of cryptocurrencies, important ongoing considerations are sure to include anti-money laundering laws, as well as know-your-customer laws that ensure financial institutions are able to verify the identities of their clients. Organizations have begun appearing to aid in this effort: in 2015, the U.S. Chamber of Digital Commerce and Coin Center came together to create the Blockchain Alliance, a non-profit that serves as forum between the blockchain industry and law enforcement and regulatory agencies.12

OUTLOOK FOR CRYPTOCURRENCY

The outlook for cryptocurrencies is far less clear than that for blockchain technology in general, and some major impediments stand in the way of widespread cryptocurrency usage. One impediment is a lack of real-world use cases. Many existing cryptocurrencies, particularly those that are less well-known, are designed to be used with a software or service that does not exist or has yet to be completed. Others may have no viable real-world use whatsoever. And even well-known currencies, like Ripple’s XRP, depend entirely on the success of the networks and businesses behind them.

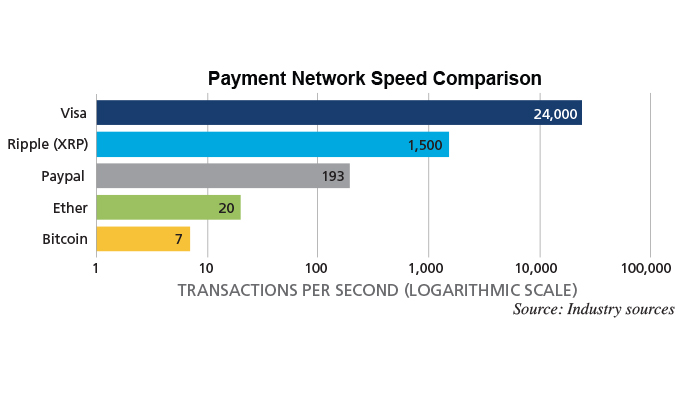

For cryptocurrencies that are designed to be used for payment networks, like Bitcoin or XRP, scalability is a primary concern. Due to the structure of conventional blockchains, high levels of traffic can bog down the networks, making transactions slow and expensive. Bitcoin in particular is known for its lack of scalability, and many other cryptocurrencies, including XRP, have attempted to improve upon Bitcoin’s transaction speeds. While some have succeeded, the transaction speeds of most cryptocurrencies still remain far below those of established payment networks like Visa’s.

Another major concern for cryptocurrencies is their potential use in criminal activities. Thefts of Bitcoin are on the rise, up from $3 million in 2013 to $89 million in 2017, according to cryptocurrency transaction analysis firm Chainanalysis Inc. While this amount is a relatively small fraction of the multi-billion dollar global Bitcoin market, incidences of cryptocurrency theft are growing rapidly. Even more concerning is the use of cryptocurrencies in illicit transactions, from online sales of illegal goods to hackers demanding untraceable cryptocurrency as ransom. Blockchain Intelligence Group Inc., a company that makes software that tracks cryptocurrency use, estimates that illegal activity accounts for about one-fifth of transactions for a group of the largest cryptocurrencies.

While regulators in the U.S. and elsewhere begin to address the issue of cryptocurrencies, other parties are also developing new technologies to help law enforcement monitor cryptocurrency usage. The governments of Japan and Russia have already announced that they have developed software that can track all cryptocurrency transactions within their borders, which they plan to use to combat fraud and money laundering.13

Other technological advancements in the cryptocurrency space could also lead to greater mainstream adoption. Recently, a variety of companies have begun developing new “stablecoins,” or cryptocurrencies whose values are pegged to currencies like the U.S. dollar or Euro. Stablecoins not only allow investors to maintain a safe store of value in the cryptocurrency space, but they could also encourage more businesses to accept cryptocurrencies as payment for goods and services. Many companies in the cryptocurrency industry are also pursuing ways to make payment networks more effective, and some, like STEEM and BitShares, now claim to be able to handle as many as ten thousand transactions per second.14 In the investing world, cryptocurrencies have already reached the mainstream in many ways, and industry giants, like Fidelity, are now creating cryptocurrency trading desks and offering custodial services for digital assets.

BLOCKCHAIN & CRYPTOCURRENCY IN INVESTMENT PORTFOLIOS

Given the dynamic regulatory environments, increasing law enforcement, and ongoing technological changes surrounding digital assets, cryptocurrency values will likely continue to be dominated by speculation for the foreseeable future. Investors in cryptocurrencies should be prepared for extreme volatility and the potential complete loss of investment principal. Therefore, cryptocurrencies and cryptocurrency investment funds are likely inappropriate for investment portfolios that target capital preservation. However, as cryptocurrency technologies and regulations evolve and stabilize, future opportunities in the space may appear.

Blockchain technology remains poised to transform many areas of the economy, and companies that are able to utilize blockchain technology in their operations or that aid other businesses in integrating blockchain technology could stand to benefit. Regardless, the blockchain industry continues to evolve rapidly, and there is no guarantee of success for new blockchain-oriented companies or technologies.

AMG will monitor the blockchain and cryptocurrency space for potential future opportunities as the technological and legal landscape continues to evolve.

Notes

-

Bitcoin pricing data sourced from CryptoCompare. https://www.cryptocompare.com/.

-

Zhao, Wolfie. South Africa’s Central Bank Claims Success in Blockchain Payment Trial. CoinDesk, 6 June 2018, www.coindesk.com/south-africas-central-bank-claims-success-in-blockchain-payment-trial/.

-

Wall Street Blockchain Alliance, www.wsba.co/.

-

Venture Capital Firms Go Deep and Wide with Blockchain Investments. Diar, 16 Oct. 2018, diar.co/volume-2-issue-39/.

-

Global cryptocurrency market capitalization data sourced from Coinmarketcap. https://coinmarketcap.com.

-

Count of global cryptocurrencies sourced from Coinmarketcap. https://coinmarketcap.com/.

-

Cryptocurrency ATM data sourced from Coin ATM Radar. https://coinatmradar.com/.

-

Bitcoin Accepted [Everyw]Here: Square Patents Crypto Payment Network. CCN, 29 Aug. 2018, www.ccn.com/bitcoin-accepted-everywhere-square-wins-patent-for-cryptocurrency-payment-network/.

-

All cryptocurrency regulation information sourced from ComplyAdvantage unless otherwise specified. https://complyadvantage.com/knowledgebase/crypto-regulations/.

-

Taxation of Cryptocurrencies in Europe. Crypto Research Report, 31 Oct. 2018, cryptoresearch.report/crypto-research/taxation-cryptocurrencies-europe/.

-

Hajric, Vildana. SEC Crypto Settlements Spur Expectations of Wider ICO Crackdown. Bloomberg, 19 Nov. 2018, www.bloomberg.com/news/articles/2018-11-19/sec-crypto-settlements-spur-expectations-of-wider-ico-crackdown.

-

Combating Criminal Activity on the Blockchain. Chamber of Digital Commerce, digitalchamber.org/initiatives/blockchain-alliance/.

-

Godshall, Jacob. Japanese Authorities to Implement Software to Track Cryptocurrency Transactions. Unhashed, 31 Aug. 2018, unhashed.com/cryptocurrency-news/japanese-authorities-software-track-cryptocurrency-transactions/.

-

Steem: An Incentivized, Blockchain-Based, Public Content Platform. Steemit Inc., June 2018, steem.com/steem-whitepaper.pdf.

Member FDIC • Non-deposit investment products: Not FDIC insured • No bank guarantee • May lose value