Since 1990, the phenomenon known as “gray divorce”—a term used to define late life divorces of individuals over the age of 50—has been on the rise.

According to an analysis of divorce data released in July 2023 by Bowling Green State University’s National Center for Family and Marriage Research, the most significant increase in divorce rates occurred with people 65 and older, which tripled from 1990 to 2021.

Longer life expectancy, becoming empty nesters, and a reduced stigma associated with baby boomer divorces are each partly behind the rising gray divorce rate. Regardless of the reasons, a gray divorce among affluent older couples comes with its own set of financial challenges that differ from a middle-age high-net-worth divorce.

Gray divorce issues include untangling potentially complex finances, property division (including the marital home), the disruption to retirement plans, less earning potential, spousal maintenance, estate planning and beneficiary designations.

Gray divorce can be especially difficult for women: They are more likely than men to emerge from gray divorces in an economically disadvantaged position.

Engage Expert Financial and Legal Counsel

Assembling a team of experts is essential to safeguard assets and lay the groundwork for a secure post-divorce future. Consider including:

- Divorce Attorneys Specializing in High Net-Worth Individuals. Your divorce attorney should be adept at negotiating and litigating issues such as complex marital property division.

- Financial Advisor. Your attorney can help you achieve what you deserve, but a financial advisor can evaluate and explain the long-term impact of settlement options along with restructuring your financial plan to avoid post-divorce financial challenges.

- Tax Advisor. Your accountant can help you optimize for tax impact when deciding on the equitable split of marital property.

- Estate Planning Attorney. Your estate planning attorney can help with updating documents such as will, trusts, powers of attorney, and medical directives to protect your legacy and make sure your assets are distributed to the individuals and organizations you wish.

The Full Extent of Your Financial Picture

Splitting marital property

Individuals exiting long-term marriages may not have the benefit of a prenuptial agreement but likely have finances, assets, and debt that are deeply entwined, necessitating a clear understanding of whether assets are marital property or separate.

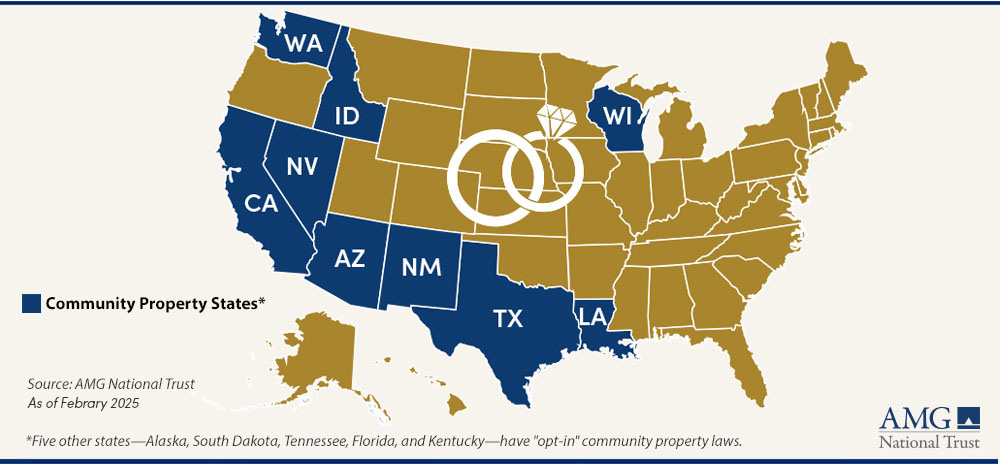

The approach to asset division depends on whether the state where you reside is an equitable distribution state or a community property state.

In equitable distribution, the court will aim to divide assets in a manner deemed to be “fair,” which doesn’t necessarily mean equally. This approach generally involves looking at things like the financial needs of each individual, contributions to the marriage, duration of the marriage, age and health of both spouses, and employability and earning power.

Conversely, a community property state will look to divide assets 50/50. Also, it’s possible that a divorcing couple can come to their own agreement on the division of assets.

Dividing debt acquired during marriage

Like assets, it’s important to determine whether debts are marital or separate.

Considering the type of asset and available income stream to service the debt will be important in negotiating the division of debt as well as identifying which debts are or should be considered jointly owned and the responsibility of each spouse. It’s important to know that legal responsibility for the debt does not always align with the person whose name may be on the account.

Dividing debt requires careful analysis, strategic negotiation, and a clear understanding of legal and financial implications. Engaging with divorce lawyers and financial advisors to guide you through this process can help see that debts are divided fairly and that your financial health is protected post-divorce.