Analyze Possible Divorce Settlement Options

The equitable distribution of marital property does not necessarily mean a simple 50-50 division of each asset between spouses.

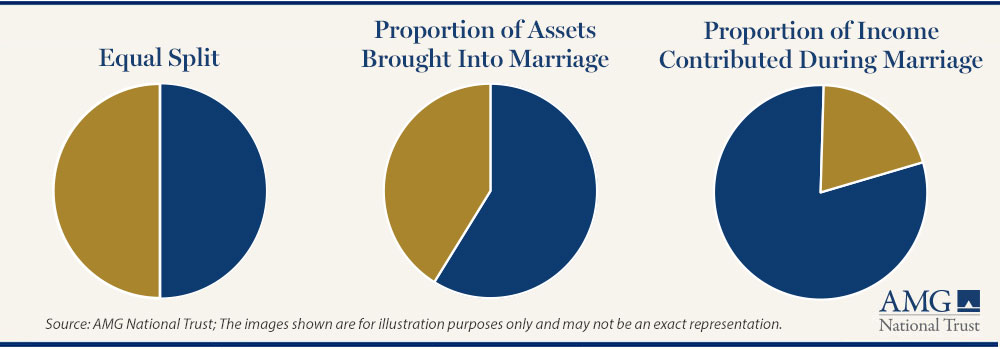

It could involve a discussion of the fair market value of total marital property, what the equitable division of it might be, and then allocating specific assets. A fair division of assets and liabilities could be 50-50, a proportion of what each side brought into the marriage, or perhaps a split based on the annual income contributed to the marital household.

50-50 split not always wise

Did you come into marriage with equal assets or did one partner bring significantly higher wealth or debts? If you put a promising career on hold to raise children or to accommodate your spouse’s employment, you likely don’t want to be left with less than what you started with.

Your advisors will likely want to dig deeper into key financial records and consider what type of assets are being talked about, such as property, retirement savings, stock options and other executive compensation benefits—and any taxes tied to those assets.

When working to settle the division of assets in your marriage, it can be helpful to forecast your future income and spending needs as independent households. These expectations also can inform petitions for alimony and child support.

Other important considerations include:

- Is there something that you brought into the marriage that you want to retain?

- Is there a marital asset to which you contributed more toward?

- Are some assets riskier than others?

- What are your liquidity and cash flow needs? Agreeing to accept future benefits such as Social Security, pension or other retirement accounts won’t put money in your pocket today.

Although a prolonged divorce can be costly, be careful in making quick decisions to speed up the divorce process. The desire to move things along quickly is understandable, but the risk to your financial future is that you are giving away something you shouldn’t or are accepting something without fully understanding the implications.

Tax implications buried in each decision

Selling, transferring, or splitting an asset often has important personal tax implications, particularly when they involve higher amounts of wealth or complicated compensation structures.

Because taxes can erode the value of the assets a party receives, it is crucial to understand whether the value that appears reasonable at first glance is the pre-tax or after-tax value. For example, $100,000 in a traditional retirement account is not the same as $100,000 in a Roth retirement account because the former is taxable at withdrawal and the latter is not.

Likewise, consider whether to accept homes or other properties based on their current value and the potential capital gain or loss if you were to sell, or how to handle investments in a brokerage account considering potential tax consequences for gains above the cost basis.

Your financial advisor can examine each asset and liability and present you with options to optimize your tax efficiency during and after the divorce.

State laws governing divorce proceedings

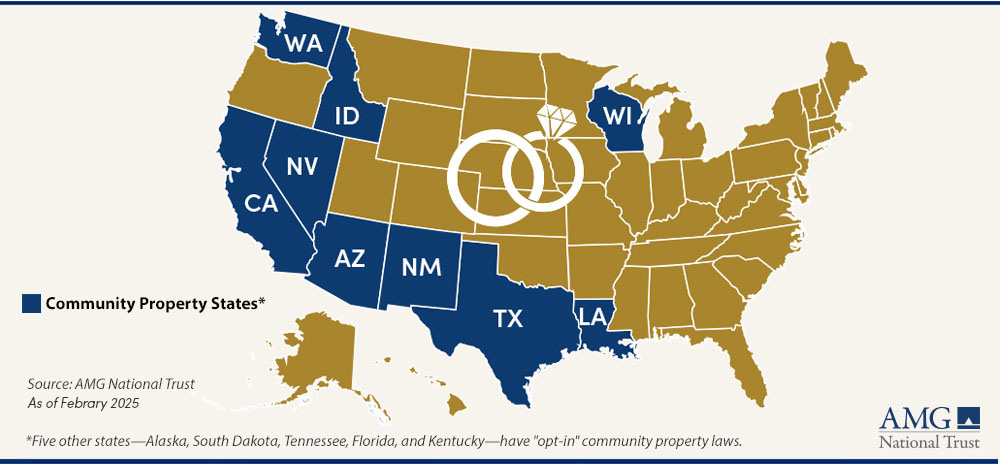

When spouses are unable to agree on a divorce settlement, the laws in each state generally kick in. If you live in one of the nine community property states, an asset or liability may be considered the equal property of both parties if acquired during marriage, with some exceptions.

The majority of states are common law property states where an asset or liability is generally the property of the person to whom it is titled regardless of when it was acquired. These states distribute marital property based on an agreement of the parties or in a manner that the court deems “fair” to both parties, but not necessarily equal. This is called “equitable distribution.”

However, some assets already may have been shielded from a divorce settlement.

- Trust. A high-net-worth family may choose to protect its financial interests through a trust. Depending on the type and trust terms, assets held in a trust may remain separate from marital property so long as they were not commingled during marriage. Your advisors likely would want to trace the source of assets into the trust to help accurately determine which assets could be considered marital property.

- Prenup. A prenuptial agreement also can remove specific assets from marital property, specify the amount and length of alimony to be paid in the event of divorce, and discuss custody and child support issues. Certain conditions must be met for a prenup to be considered valid during the divorce process.

Update Your Estate Plan

Do you want your former spouse to remain as the primary beneficiary on your retirement accounts, investment accounts, bank accounts, insurance policies, pension, or any other element of your estate plan?

Divorce generally does not force any automatic changes to beneficiary designations, nor does it prevent you from keeping a former spouse as a beneficiary. The choice is yours, though your decision should reflect your new life rather than the past.

After the divorce decree, you, and potentially your advisors, should retain a copy of the settlement to be aware of any obligations you continue to have to your former partner.

Also consider reviewing these items:

- A will, because divorce can alter or void some provisions

- A trust, particularly if it held marital property that was included in the settlement

- Healthcare power of attorney

- Guardianship of minor children

- If you are planning to remarry, consider a prenup to safeguard assets for children from a previous relationship or to clarify payments to a previous partner.

PARTNER WITH AMG AND START BUILDING YOUR FUTURE

Divorce negotiations can seem never-ending, but having a trusted financial advisor and comprehensive wealth manager by your side can help. Our role as part of your team is to help make it more manageable by identifying key financial decisions and potential risks, while also modeling various scenarios to help explain the financial trade-offs of each decision.

If you are almost through the divorce process, ensure your advisor can facilitate your next steps—a partner that understands your financial goals and evolves as you do. AMG’s comprehensive solutions seamlessly connect every aspect of our firm—wealth management, taxes, philanthropy, retirement planning, and more—to deliver toward your success.

If you would like to schedule a free consultation with AMG about financial security after divorce, call 800-999-2190 or email with the best day and time to reach you.