EXECUTIVE SUMMARY

The bull market in U.S. stocks that began in 2009, now one of the longest in history, has been dominated by high returns, low volatility and few major price corrections. This environment has been a boon for passive index funds that simply buy and hold stocks, but it has also made it difficult for active managers—fund managers that aim to select top companies and protect against market declines—to beat passive indices like the S&P 500.

Supporters of passive investing have been quick to write the obituary for active management, and it is true that trends such as a concentration of assets in the largest actively-managed funds could represent headwinds for the industry. However, active managers have historically been able to outperform passive indices in periods when stock market returns are low, negative or experiencing higher volatility.

More importantly, top-performing active managers have shown the ability to match or beat passive benchmarks over the long term. These “best-of-breed” managers share certain qualities that allow them to outperform over time and under different market conditions. AMG has developed a rigorous manager selection process to determine which managers fall in this category.

This report explores the current active management environment, the historical relationship between active management performance and stock market returns, and the key characteristics AMG uses to identify best-of-breed active managers.

A CHALLENGING ENVIRONMENT

A variety of economic and market factors combined to produce a difficult environment for active managers in recent years. The U.S. economy has grown steadily and in a broad-based fashion as industries have recovered from the Great Recession. The U.S. Federal Reserve has buoyed stocks by maintaining record-low interest rates and making direct market purchases of debt and mortgage-backed securities, also known as quantitative easing. Volatility across asset classes has been historically low, helping to support high valuations.

Together, these factors have allowed for impressive returns in the U.S. stock market, but have also resulted in a lack of discrimination between stronger companies or industries and weaker ones. Quantitative easing and record-low interest rates have acted as a “rising tide that lifts all boats”, reducing the effectiveness of key active management skills like stock picking and industry rotation. Low volatility and a lack of meaningful price corrections have also made it difficult for active managers to profit from market timing.

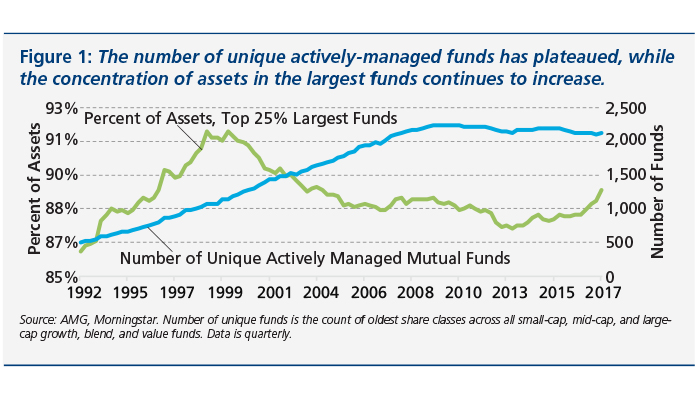

There are also trends within the active management industry itself that may be contributing to declining quality for the median active manager. For example, the number of unique mutual funds has declined since 2009, while the largest funds have grown in recent years (Figure 1). An increase in the number and size of large funds could be a negative for total actively-managed fund returns, as research suggests that mutual funds that stop taking assets before they grow too large tend to outperform their larger peers.1

Domestic stock mutual funds also appear to be hugging their respective benchmarks more closely than in the past, with a three-year tracking error (a measure of how much a fund’s returns differ from its passive benchmark’s returns) declining from around 10% in 2001 to just 4% in 2017, according to data from Morningstar. Studies have found that funds that are less willing to differentiate from their benchmarks are less likely to outperform2 those benchmarks, so the decline in total tracking error may also result in lower returns for the average mutual fund.

However, at this late stage of the economic cycle it can be easy to forget that the majority of periods in the stock market’s history have had consistently higher volatility and more frequent price corrections than seen today. Under those conditions, active management adds greater value.

ADVANTAGES OF ACTIVE MANAGEMENT

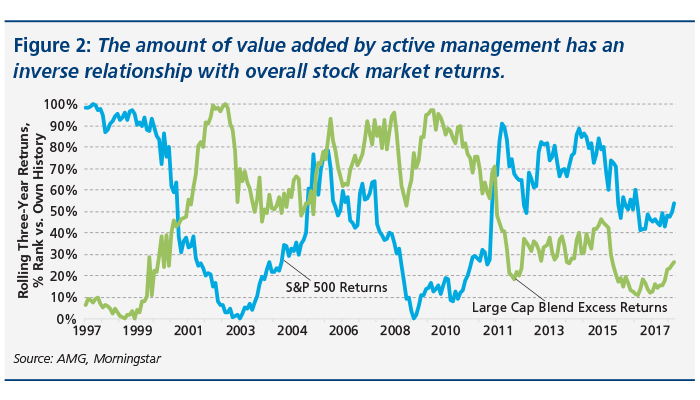

The headwinds facing active managers and the challenging state of the market have led many to question whether there is still value in investing in actively-managed funds. In reality, active management tends to perform best versus passive management when the stock market is experiencing low returns, falling prices or high volatility. Tough market conditions like these allow active managers to add value by moving money into cash, rotating to stronger companies or industries and taking advantage of pullbacks to buy undervalued shares. Over time, this relationship has resulted in an inverse association between broad stock market performance and active managers’ excess returns—or returns in excess of their benchmarks (Figure 2).

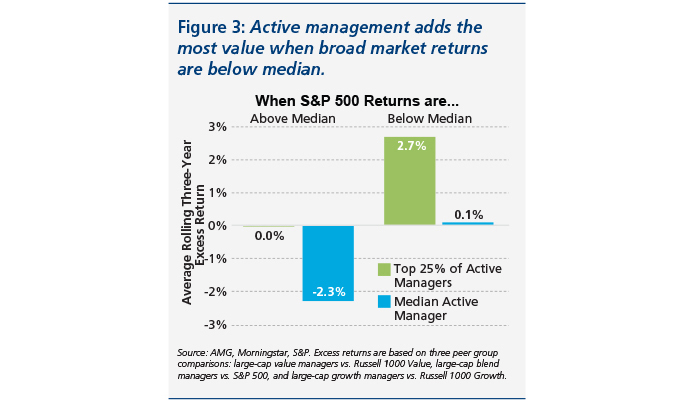

Another way of looking at the relationship between market returns and relative active manager performance is to determine how active managers have performed when S&P 500 returns are either above or below the historical median. For example, from Oct. 1992 to Oct. 2017, the median rolling three-year return for the S&P 500 was 11.8% annualized, based on S&P data. As Figure 3 shows, in periods when the S&P 500’s three-year rolling return was higher than 11.8%, the median active manager underperformed by 2.3% and even top active managers merely matched the market’s performance. However, in periods when the S&P 500’s return was below 11.8%, the median active manager beat the benchmark and top quartile active managers outperformed the benchmark by 2.7% per year on average. This suggests that active management can add value in times of lower market returns.

Active management has also historically outperformed passive indices during price corrections and in periods of market drawdowns. For example, the S&P 500 has had 21 major drawdowns of 10% or greater since 1987, based on data from S&P. Of the 21 periods, large cap blend active managers outperformed the S&P 500 in 12 of those periods and had average excess returns of 1.2% over all drawdown periods. These results indicate that active management may also play a role in protecting against broad market declines.

TOP ACTIVE MANAGERS OUTPERFORM

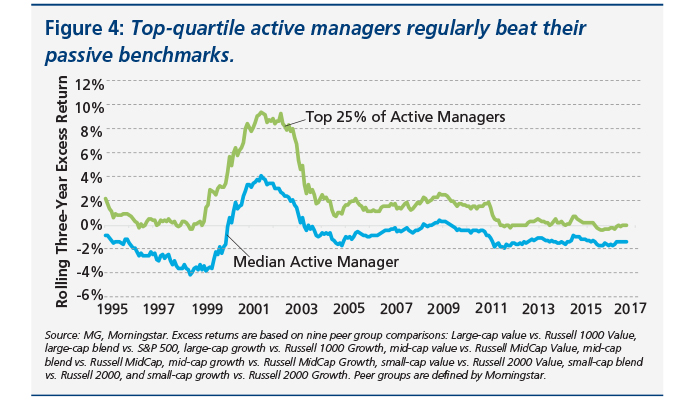

Despite the value active management can provide a portfolio during market drawdowns and when broad market returns are low, the median active manager has historically failed to consistently beat a passive benchmark over longer time periods. Figure 4 illustrates the relative performance of the median active mutual fund versus its applicable passive benchmark since 1995, as well as the relative performance of funds that fall in the top 25% of all performers.

As the figure shows, median actively-managed mutual funds underperformed their passive benchmarks on a running three-year average basis for the majority of the period in question. Top-quartile funds, on the other hand, have been able to beat their passive benchmarks for most of the last two decades, and added particular value during the equity bear markets of 2002 and 2008. Thus, in order to benefit from active management over the long term, it is essential to be able to identify top-performing funds.

FOCUS ON THE BEST-OF-BREED

AMG uses a variety of quantitative and qualitative criteria when evaluating investment managers to identify funds that can add value to a portfolio over time and under different market conditions.

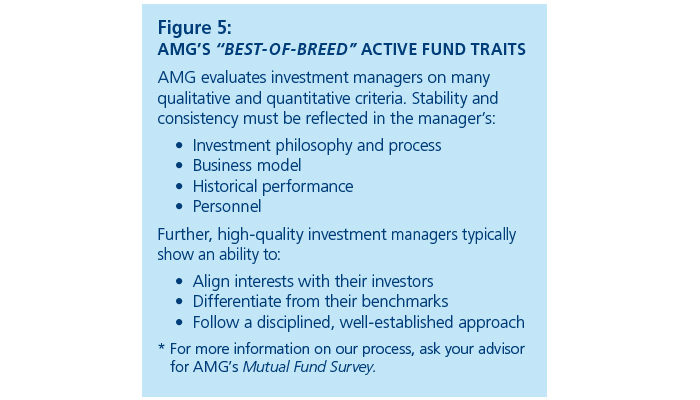

As shown in Figure 5, there are certain traits shared by top active managers. These best-of-breed characteristics are representative of managers that not only have strong historical performance, but also have proven the ability to craft and adhere to a successful investment philosophy over time.

Top active managers tend to have established and proven business models, and the experienced and qualified personnel necessary to execute on their investment philosophies. AMG typically looks for portfolio managers with tenure and strong track records in a given area of expertise.

The most effective active managers also typically align their business models and fee schedules with the interests of investors, ensuring that the managers have a vested interest in performing well for their clients. These firms are often willing to differentiate from their benchmarks as they seek to minimize risk and maximize returns across market cycles.

AMG ADHERES TO A PROCESS

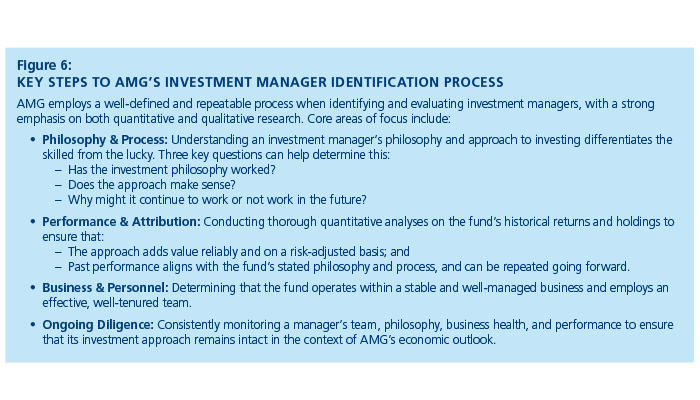

In order to find high-quality investment managers, AMG believes a disciplined process is necessary. This involves knowing what criteria to seek out and knowing what questions to ask when evaluating a manager. Beyond the best-of-breed traits mentioned in the previous section, AMG looks for factors including employee ownership of a mutual fund, the focus of the fund’s parent corporation and the willingness of a fund to stop taking assets when it no longer perceives opportunities in the market.

AMG’s manager identification process is based on the traits that characterize the most successful and consistent actively-managed funds, from commitment to a proven investment philosophy to the employment of experienced personnel. Key steps to this process are listed in Figure 6.

Historically, the median active manager has not been able to add value beyond that of an applicable passive index. AMG’s rigorous investment manager identification process helps to identify the active managers that not only have the potential to beat passive indices during stock market drawdowns, but also over time and in different market environments.

Given the current state of high U.S. stock market valuations and the extended outperformance of passive index funds, AMG believes incorporating best-of-breed active management in a portfolio could help protect against market declines and improve returns over the long term.

Contact your AMG advisor for more information on how your portfolio might be able to benefit from active management.