Reality of Illiquid Assets

High net worth often brings opportunity—and complexity. In fact, wealth is often created through at least some planned illiquidity—a concentrated stock position, inheritance, or having your own business. As wealth grows, your financial planning will likely aim to diversify it across a wider range of assets, including illiquid investments such as a family business, commercial or residential real estate investing, private equity, venture capital, fine art, or collectibles.

These assets could have a high appraised value, but converting that value to a liquid (e.g., cash) asset may take considerable time and effort. For example, a business sale may require months or years of preparation, negotiation, and due diligence, and the process can be especially demanding if waiting too long to act leads to rushed decisions. Real estate transactions can be slowed by market conditions, financing constraints, or regulatory hurdles. Private investments often include lock-up periods or limited secondary markets. Even high-value collectibles or fine art depend on finding the right buyer at the right time. At the point when liquidity is needed most—such as after a death or major event—illiquid assets, like real estate, can create significant challenges for heirs, who may need to sell these assets quickly to cover estate tax obligations.

The ultimate goal is to ensure that a long-term care event is paid for through a structured plan that maximizes tax efficiency and preserves the overall estate and wealth transfer goals.

Care Costs Continue to Rise

Planning ahead for the cost of long-term care requires an acknowledgement that treatment could become progressively more intensive and expensive, with little certainty about how the course of an illness or care requirements will change over time. The cost can be above $100,000 per year for higher levels of care, such as for a private room in a nursing home facility. Also consider that the cost of care continues to rise—total U.S. health expenditures reached about $4.8 trillion in 2023, more than triple the amount from two decades earlier.

For those who don’t think it can happen to them, an estimated 56% of Americans turning 65 between 2021 and 2025 are likely to experience a long-term care event, according to a recent federal study. Relying on hope alone for care planning is risky; proactive strategies are essential to address these likely needs.

Medical care is often compounded by comorbidity issues that increase needs for health care services such as diagnostics, medications, hospitalizations, and specialized care.

Attitudes toward care planning can be shaped by experiences and perceptions formed in the early years, influencing how individuals approach these decisions later in life.

Aging also impacts the cost, but not equally. The average life expectancy for U.S. women is 80.2 years, as of 2022. That’s nearly six years longer than for men. (These numbers are an increase over 2021 but do not fully offset a decline during the COVID-19 pandemic.) As women continue to outlive men, they are more likely to live at home when they are older and may need care services for longer. Proactive life care planning allows for home modifications that enable aging in place, often a preferred but expensive option.

Tax Drag Can Undermine Liquidity

Tax drag refers to the impact of taxes on investment returns, such as capital gains, dividends, and interest income. Over time, that reduces how much of a portfolio is available to compound—and how much is readily accessible when cash needs arise.

This becomes especially important in the context of long-term care. For many investors, liquidity must be created by selling appreciated assets—whether from a stock position, a business interest, or real estate. The result: a meaningful portion of the proceeds can be lost to tax drag at precisely the moment funds are needed. In addition to triggering significant capital gains, selling appreciated assets to pay for care can also eliminate a step-up in basis for heirs.

Preparations and Potential Safeguards

The solution is not necessarily reducing exposure to illiquid assets but ensuring that sufficient liquidity exists elsewhere in the financial plan. It is critical to work with your financial advisor early on to develop a strategy that reflects your values with respect to your care and your estate plan.

Below are some options that AMG includes in discussions with clients to get a sense of preferred ways to meet their unique needs.

Long-Term Care Insurance

Traditional, private health insurance may not cover assisted-living or similar long-term care, though providers may cover some medical services within such a facility. In response, long-term care insurance (LTCI) has evolved to be similar to some life, home, or auto policies—offering a range of policy options where you can choose the coverage that fits your circumstances.

For high-net-worth families, LTCI could be considered more of a liquidity planning tool than as risk protection—protecting the balance sheet while maintaining flexibility.

LTCI also generally has a use-it-or-lose-it structure, meaning that if long-term care services are never needed, you do not get any money back. Policies typically kick in when the policyholder is unable to perform at least two activities of daily living and can pay for in-home care, nursing home stays, adult day care, and assisted living facilities.

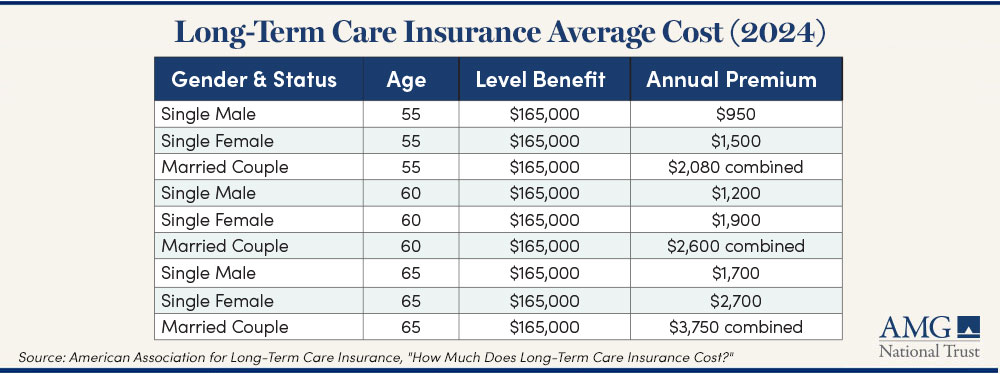

The level of coverage and your age are among the factors that determine the monthly policy premium you pay the provider.

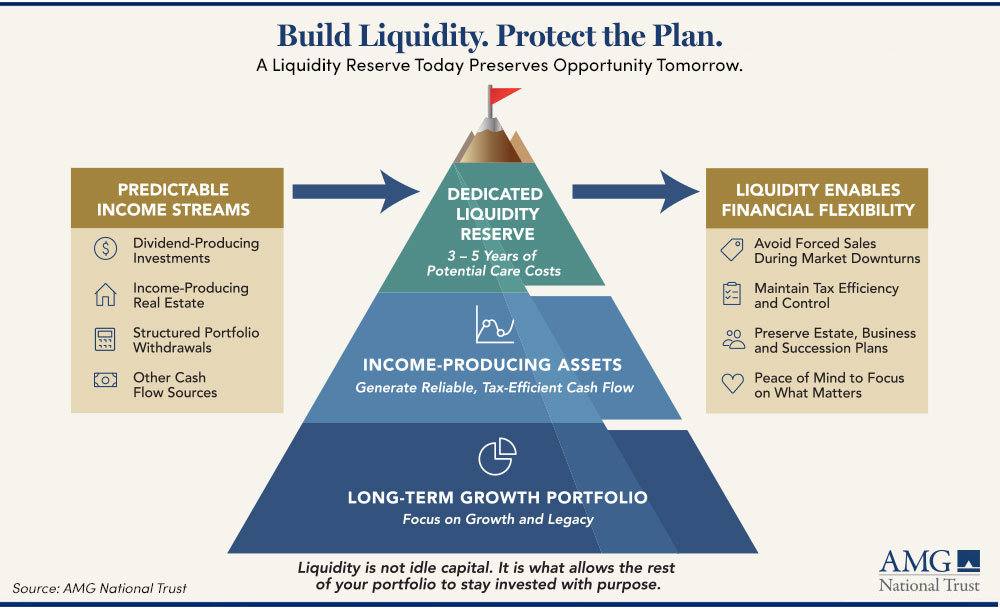

Self-insuring involves using your own resources to build a financial cushion for care or other unexpected needs. This means building a liquidity reserve within the overall financial plan—assets that can be accessed quickly without forcing the sale of a business, real estate, or long-term investments. Many high-net-worth individuals establish dedicated liquidity reserves specifically to cover 3–5 years of potential care costs, which helps prevent the need to liquidate long-term growth investments.

Self-insuring involves using your own resources to build a financial cushion for care or other unexpected needs. This means building a liquidity reserve within the overall financial plan—assets that can be accessed quickly without forcing the sale of a business, real estate, or long-term investments. Many high-net-worth individuals establish dedicated liquidity reserves specifically to cover 3–5 years of potential care costs, which helps prevent the need to liquidate long-term growth investments.