• 2 min read

Sign up to receive a weekly email summary of new articles posted to AMG Research & Insights.

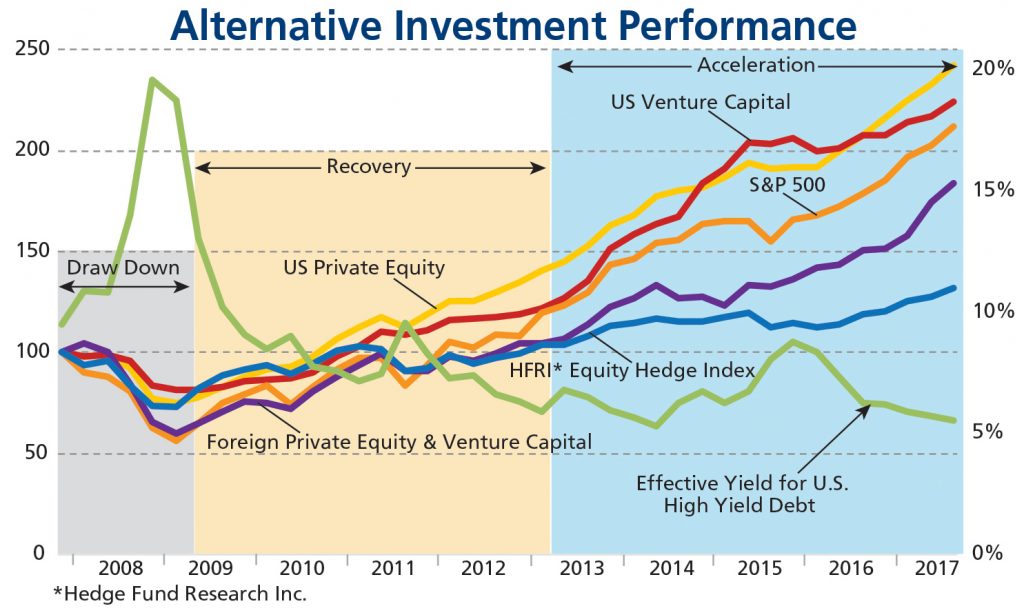

Alternative assets have exhibited very different return characteristics from public equities since the 2007 financial crisis.

A decade ago, massive declines in financial assets and movement in asset-class prices were highly correlated, yet alternative strategies served to protect capital against some of the declines. Hedge funds protected on the downside as expected, but private equity proved surprisingly resilient and early-stage venture-capital investors saw many of their companies grow throughout the downturn.

The drawdown’s severity brought many fears into play, and it seemed at times that the losses were insurmountable. Nevertheless, most assets began a long trudge to recovery, and investments that suffered the least declines were quickest to recover, with hedge funds, U.S. private equity and venture capital leading the way. Public equities, including the S&P 500, took much longer to regain their prior high-water mark.

Over the past 11 years policymakers have used near-zero interest rates and quantitative-easing strategies to drive liquidity back into the market, leading to asset-price appreciation and accelerated returns for many assets. Any hedge on the market held back returns, but venture-capital and private equity investments in the United States did quite well.

This all suggests that a well-diversified portfolio that includes alternative assets helps protect capital during a market sell-off, but also participates in returns, while asset prices recover.

This information is for general information use only. It is not tailored to any specific situation, is not intended to be investment, tax, financial, legal, or other advice and should not be relied on as such. AMG’s opinions are subject to change without notice, and this report may not be updated to reflect changes in opinion. Forecasts, estimates, and certain other information contained herein are based on proprietary research and should not be considered investment advice or a recommendation to buy, sell or hold any particular security, strategy, or investment product.

Sign up to receive a weekly email summary of new articles posted to AMG Research & Insights.