Should investors worry that America will default on its financial obligations sometime this year, plunging economies and markets worldwide into chaos?

Probably not, but it’s a fair question. The new Republican majority in the House of Representatives is threatening to reject an increase in the U.S. debt limit unless President Biden cuts government spending. Both sides seem intransigent.

The real issue isn’t the current debt limit, which must be increased for the government to pay its bills; it’s America’s exploding national debt of $31 trillion, which is more than 120% the annual U.S. GDP of $25 trillion. Two decades ago, most economists would have declared that irresponsible financial management, befitting a developing country, not one of the world’s most advanced economies.

Here’s some perspective: In 1929, when GDP measurements started, U.S. economic output was $105 billion and the national debt was $17 billion or 16% of GDP. In 2000, GDP was $10.25 trillion, and the national debt was $5.7 trillion or 56% of GDP. Over the past 20 years, America’s GDP has more than doubled, but the national debt has increased more than fivefold.

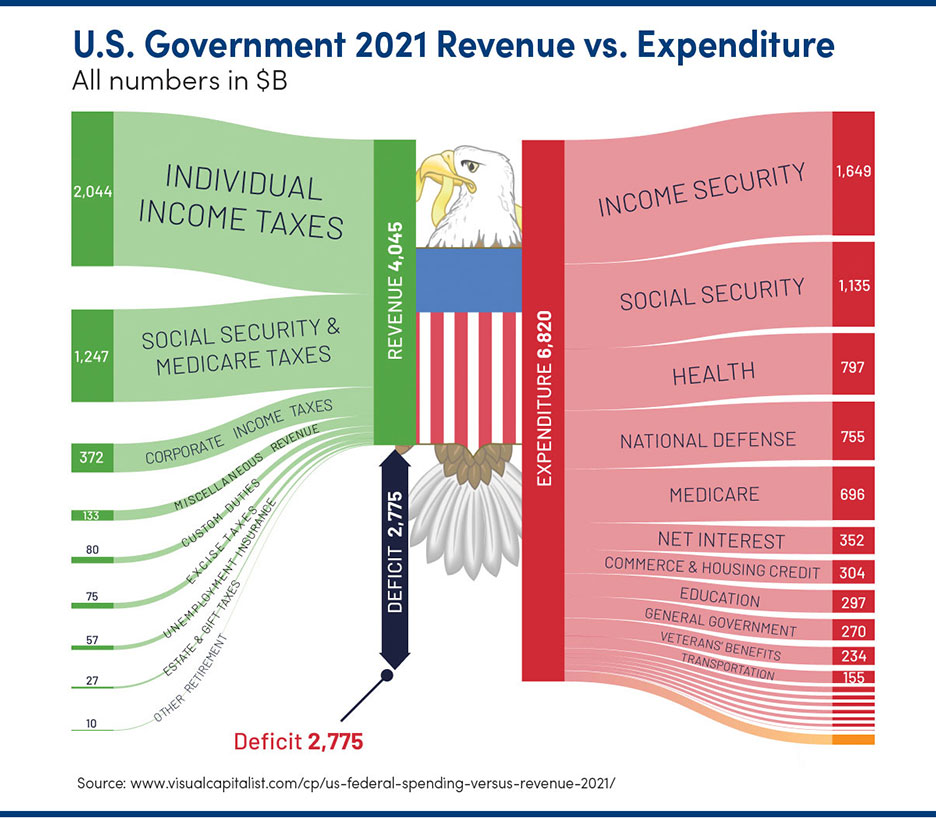

The graphic below shows recent federal budget outlays:

Note that entitlements and interest paid on national debt represent roughly 70% of the federal budget. Neither of these are negotiable. Modifying entitlements such as Social Security and Medicare/Medicaid would require major legislative changes, which is highly unlikely in the current era of political polarization.

Interest to be paid is determined by our growing national debt with interest rates being dictated by the financial markets. The latter has become an issue. If interest rates rise 1% to 2% higher than they have in the past decade, the annual interest cost of our national debt could increase to 7% or more over the next five years. This would result in either higher deficits or cuts in discretionary government spending on the military, transportation projects and foreign aid, as well as education, housing and agriculture subsidies.

According to a Congressional Budget Office analysis, if current budgetary trends continue, the national debt will be equal to 215% of U.S. GDP by 2050.

Should investors worry? Some observers contend that the deficit and national debt’s size aren’t that important in the modern world. But AMG disagrees. At the very least, everyone should be aware of the potential consequences.

The National Bureau of Economic Research contends that a growing national debt will curtail economic growth because it gobbles up a larger and larger share of the nation’s available capital, increasing its overall cost, which means less and less capital is available for free enterprise. A financial crisis is averted only as long as the public (including foreigners) continue buying U.S. debt. The risk that the public won’t buy the debt increases as the debt grows as a percent of GDP.

But all of this comes at a personal cost. We are passing our national debt onto our children and grandchildren. And in doing so, we are increasing their financial uncertainty and making it harder for them to successfully build their futures.