EXECUTIVE SUMMARY

With bond yields continuing to fall this year and equity dividend yields staying relatively stable, some income-oriented investors wonder if focusing on high-dividend-yield equities can help pick up the slack. While many companies have good histories of paying out consistent dividends, investing in such companies does not necessarily improve a portfolio’s optimal cash flow, total return or risk. This is because cash flows can be generated through a wide range of sources, including dividends, share buybacks, and realized capital gains from sales. In this white paper, we highlight why focusing on after-tax total portfolio return usually leads to better results than searching just for high-dividend yield.

GENERATING INCOME IN A TOTAL RETURN FRAMEWORK

Purchasing stocks based on a small set of criteria, such as high-dividend yield, may result in a suboptimal allocation when compared to investing in stocks based on a more holistic Total Return framework by ignoring other key elements of Total Return, such as capital appreciation and share buybacks. Even a small reduction in expected Total Return can result in significantly different outcomes for an investor.

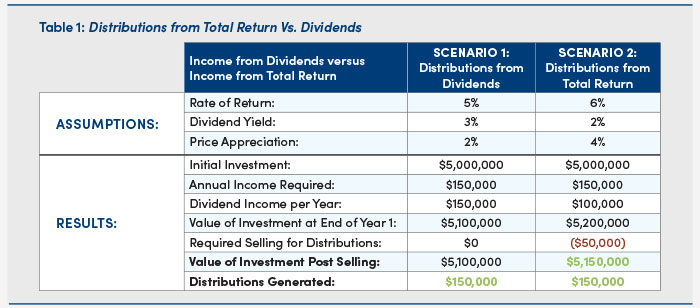

Table 1 demonstrates the impact of moving from a Total Return of 5% (and a dividend yield of 3%) to 6% (with a dividend yield of 2%)1. For a portfolio with a starting value of $5 million, a 1% increase in Total Return translates into $50,000 in more wealth generation and the same ability to generate $150,000 in cash receipts. Alternatively, this $50,000 could be used for additional distributions, and the investor ends up in the same spot in terms of wealth generation, but $200,000 in cash receipts.

DIVIDEND-PAYING EQUITIES HAVE EXTRA RISKS

By tilting to high-dividend-yielding equities, the risk profile of a portfolio could change in unintended ways that could create extra risks.

Valuation and Duration Risks

A focus on dividend yield can cause potentially unintended changes to an investor’s equity allocation. It may help to review two prominent categories of dividend-yield-oriented strategies.

High-Dividend: High-dividend strategies focus on stocks with high-dividend yields. There are different approaches: some select the highest forecasted dividend stocks, some use trailing dividend yield, some weight stocks by dividend yield, and others by market capitalization. The Dow Jones U.S. Select Dividend Index is one of the oldest indices in this space that generally tracks the performance of high-dividend-yield U.S. stocks.

Dividend-Growth: Dividend-growth strategies invest in companies with a long history of both paying and steadily increasing their dividends. The S&P 500 Dividend Aristocrats Index is a popular version of this, which includes companies in the S&P 500 with a track record of increasing dividends for at least 25 consecutive years.

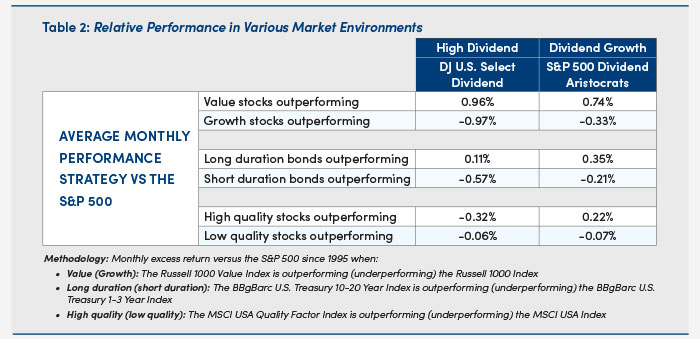

Table 2 (below) shows how these two popular dividend-oriented strategies have performed relative to broader equity markets over the past 15 years in various market environments. High-dividend strategies, as proxied by the Dow Jones U.S. Select Dividend Index, often outperform the broader equity market when value, duration, and low-quality stocks are outperforming. Dividend-growth strategies, as proxied by the S&P 500 Dividend Aristocrats Index, do best when value, duration, and high-quality stocks are outperforming.

While these factor tilts may be preferred at times, it’s important for investors to understand what risks they are taking on when investing in yield-focused strategies. Further, these factor tilts may be more effectively achieved through more direct investment approaches than a dividend-focused strategy.

Drawdown Risks

It may be tempting to rotate from fixed income securities into high-dividend-yield equities to generate greater income. However, this would likely significantly increase the drawdown risk and standard deviation of the portfolio. Doing so also negates the diversification benefits of owning high-quality bonds, such as reduced volatility and smaller drawdowns.

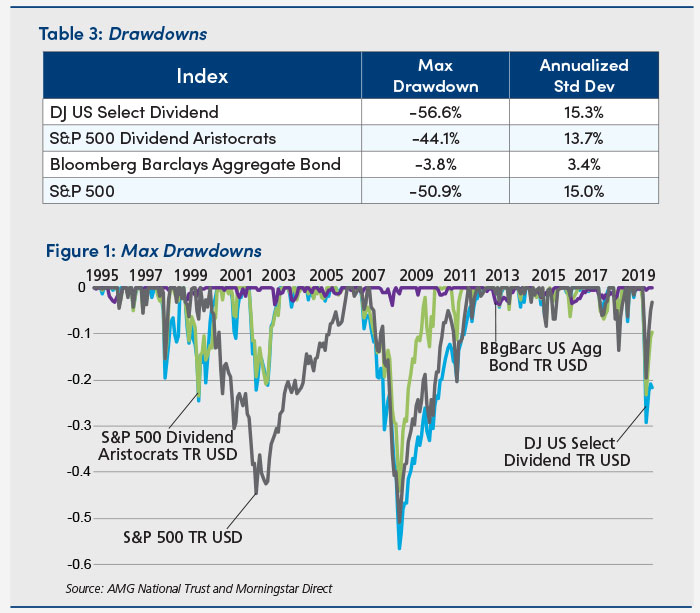

Table 3 and Figure 1 (below) show drawdowns for the Dow Jones U.S. Select Dividend, the S&P 500 Dividend Aristocrats Index, the Bloomberg Barclays Aggregate Bond Index, and the S&P 500 Index for 1995-2019. These dividend-yield strategies all have drawdowns comparable to those of the S&P 500, whose max drawdown was 50.9% during the Great Financial Crisis. Bonds had a max drawdown of just 3.8%. Standard deviation is comparable amongst the equity strategies as well. These results highlight the risk an investor takes when they transfer bond allocations into dividend-yield-oriented strategies.

PASSIVE INCOME IS CONVENIENT FOR SOME

Passive income can be a convenient source of cash for some investors. For example, investors managing their own accounts may not have the time or interest to actively liquidate holdings to generate required cash. Dividend-yielding equities can be an easy way to generate cash passively.

However, investors with a financial advisor can take advantage of a financial advisor’s expertise in managing their clients’ cash flow needs and meeting their risk and return goals. In this relationship, the convenience of passive income is no longer a significant factor.

TAXES COUNT

Taxes are important, which is why it’s critical to look at Total Return on an after-tax basis. In today’s tax environment, looking at taxes is a bit easier because qualified dividends (those received from most U.S. companies) are taxed at 20% for individuals in the highest income brackets, and long-term capital gains are taxed at the same rate for the same investors.

In this tax regime, investors can be agnostic as to whether distributions are generated from dividends, capital gains or the sale of appreciated assets. The source of the distribution is irrelevant.2

What about in a different tax regime, where the tax rate on capital gains and dividends differ? Market pricing likely would adjust to this change in tax policy. Companies also would likely adjust their dividend payout policies to better suit their equity holders. However, there may be opportunities in a more complex tax regime for specific strategies to add value based on stock selection and an understanding of the tax status of their investors. One always needs to keep an eye on taxes.

CONCLUSION

Even in a low bond yield environment, the focus should remain on Total Return for the desired risk instead of searching just for dividend yield as income can be effectively generated in a Total Return framework. While it may be counterintuitive to think of a Total Return framework as generating more income than a dividend-yield framework, understanding the multiple ways that cash flows can be generated may result in superior results over time. Income and wealth generation can be addressed through prudent management of cash flows (coupon payments, dividends, buybacks, etc.) and selling of assets.