In AMG’s latest webinar recorded on June 30, Inflation & Recession—Today’s Reality & Tomorrow’s Possibilities, our team discussed the likelihood of the high inflation rate continuing and the potential for a recession as the Federal Reserve seeks to slow the U.S. economy with aggressive monetary tightening.

Data from the Department of Labor released on July 13, 2022 showed that U.S. annual consumer prices increased 1.3% from May to June and 9.1% from one year ago.

Has the June Inflation Data Altered AMG’s View on the Likelihood of a Recession in the Next 12 Months?

In short: no, not significantly.

Although the latest core Consumer Price Index (CPI) data was slightly negative to our future growth outlook, we believe the likelihood of a recession over the next year is still about 35%.

Keep in mind that:

- The latest CPI release covers a period before the Federal Open Market Committee hiked the Federal Funds Rate by 75 bps on June 15.

As such, the year-over-year 9.1% change may be considered the last data before the earnest ramping up of monetary tightening. - AMG’s forecast incorporates forward-looking indicators.

The data that AMG evaluated while constructing its outlook incorporated a likely evolution of prices in the future. - AMG’s forecast already reflects downgraded expectations of future growth, which we proactively calculated in April at the time of the Russian invasion of Ukraine.

AMG significantly scaled back economic growth expectations before consensus and because our views on the capital markets and asset allocation are informed by a medium-term perspective (i.e., 3–5 years out) rather than monthly or quarterly fluctuations. We believe that even if a shallow, narrow recession were to occur, it would not necessarily alter our medium-term outlook. - Inflation is one part of our outlook, but not the full picture.

Real economic activity—as measured by real gross domestic product—will decide the path of growth. Although the economy’s output growth has slowed since the second half of 2021, real activity—to the degree we can see in daily and weekly data—is holding steady and not collapsing into recessionary territory. The labor market, too, remains robust. In June the U.S. economy created 372,000 nonfarm payroll jobs while the unemployment rate stayed at near-historic lows of 3.6%.

Was the Latest CPI Data in Line With AMG’s Published Outlook?

In the Q2 2022 Notes on the Economy, printed in May, we said:

“Consumer inflation patterns are expected to unfold roughly as follows.

- Near-Term Plateau – The ongoing bottlenecks will continue to put upward pressure on prices in the short run, but the month-over-month rates will ease and give way to gradual moderation.

- A Moderation Period – As the Fed continues to tighten its monetary stance throughout 2022, domestic inflation should decelerate to a range of 3-4% within twelve months.

- Longer-Term – Unless a protracted military engagement in Ukraine ushers in an era of deglobalization and resource protectionism, domestic inflation should remain stable and well anchored.”

The June CPI data aligns with the “near-term plateau” scenario described above.

Except for the “Transportation” and “Non-durables” components, the detail shows ongoing deceleration in month-over-month change in prices. The “Transportation” and “Non-durables” categories are relatively stubborn and slower to change as the former is held up by high energy prices while the latter is exceptionally sensitive to supply-chain bottlenecks.

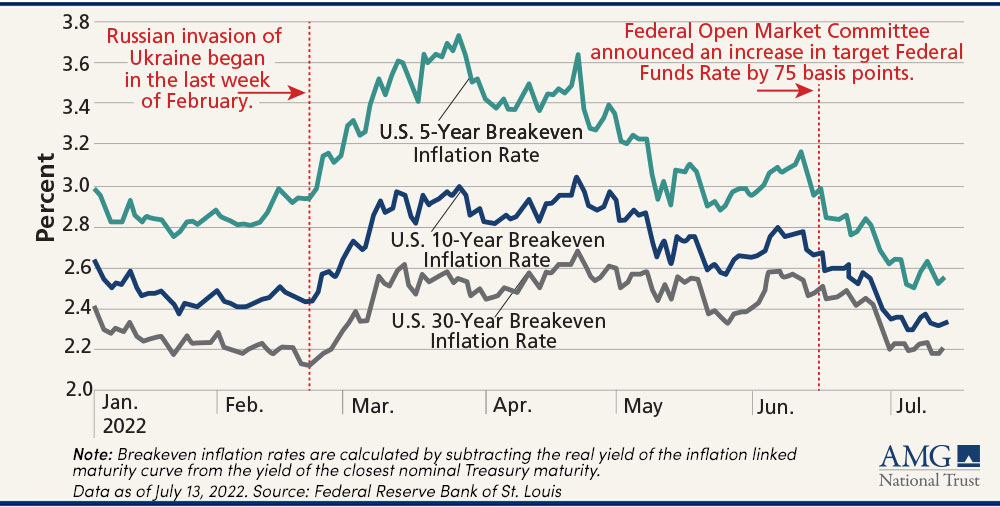

What Does the Bond Market Forecast for Future Inflation?

Breakeven inflation rates, which measure the difference between a U.S. Treasury Bond and its equivalent duration TIPS (Treasury Inflation Protected Security), spiked in response to the Russian invasion of Ukraine.

RELATED ARTICLE: THE INFLATIONARY RIPPLES OF RUSSIA’S WAR (JUNE 7, 2022)

The breakeven rates have been trending downward and continued their decline after the Federal Reserve’s 75 basis point hike in June. The breakeven rates only modestly responded to the latest CPI news.

In other words, the June data were less of a surprise than headlines would suggest and their impact on likely future inflation was much lower than the impact from Russia’s invasion of Ukraine in February.

The latest 10-year value implies that bond market participants expect inflation to be much lower in the future, 2.3%, on average, over the next 10 years.

U.S. Treasury Breakeven Rates

What Lies Ahead?

Forward-looking derivative markets continue to digest news releases and form their perspective of the likeliest path of inflation in the future.

On July 7, Fed Funds Futures implied a 97% probability of a 75 basis points hike at the Federal Open Market Committee’s July meeting. That swung up to 80% probability of a 100 basis points hike five days later. However, that has largely reversed, as of the date of this article.

A period of bumpy “retooling” for the next six to nine months is likely, but our 3- to 5-year forecast has not materially changed. We believe the economy has become more vulnerable to a recession as 2022 has progressed, but a downturn is not inevitable.

Keep an eye out: We will publish a comprehensive commentary about our outlook in the upcoming Q3 2022 Notes on the Economy in August.

In the meantime, if you have any questions, please contact your AMG advisor or call 800.999.2190.