Before the pandemic hit in spring 2020, American households regularly saved an average of 5–8% of their monthly disposable income, which is the amount U.S. residents have to spend or save, after taxes. Translated into “dollars and cents,” these monthly savings summed to around $1.5 trillion dollars, which could be used to fund future consumption.

Three rounds of pandemic-response stimulus transfers plus mobility restrictions and uncertainty about future income drastically altered American household savings.

In April 2020, when the first round of stimulus checks were sent, nearly $6.5 trillion trickled into that month’s savings—an unprecedented 33.8% of personal disposable income.

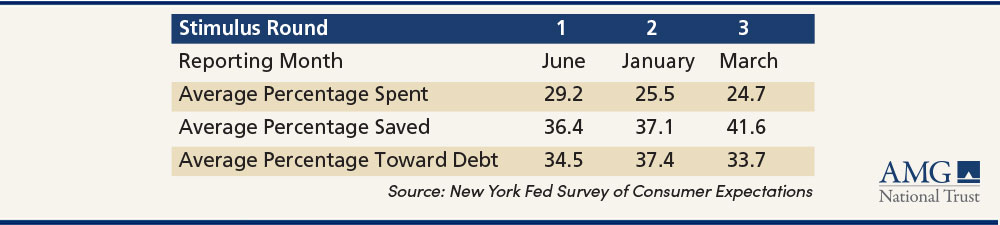

Fast forward two and a half years, we now have a good sense of how the pandemic stimulus was used by recipients:

- Roughly one-third of the money was spent within the month of receipt,

- Another one-third went toward paying down past debts, and

- Final one-third was saved.

As the pandemic dragged on and the outlook remained murky, recipients on average spent a bit less and saved more from each subsequent round. According to consumer data collected by the New York Fed, households saved 36% of the June 2020 stimulus proceeds and 42% of the March 2021 round.

How Households Used Their Stimulus Checks

Two years later, monthly savings numbers paint a different story.

In August 2022, merely $653 billion–or 3.5% of personal disposable income–were set aside. This is about 45% less than the long-run average monthly savings.

Are U.S. households now at risk of depleting their savings?

Not exactly, because the cumulative “stash” of capital to which monthly savings flow is still largely intact.

These cumulative savings, known as household total net worth, have grown. American households’ economic resources are still strong and, by extension, so is their near-term solvency.

Today, American households in general are not showing signs of running out of money or experiencing financial distress at higher-than-normal rates.

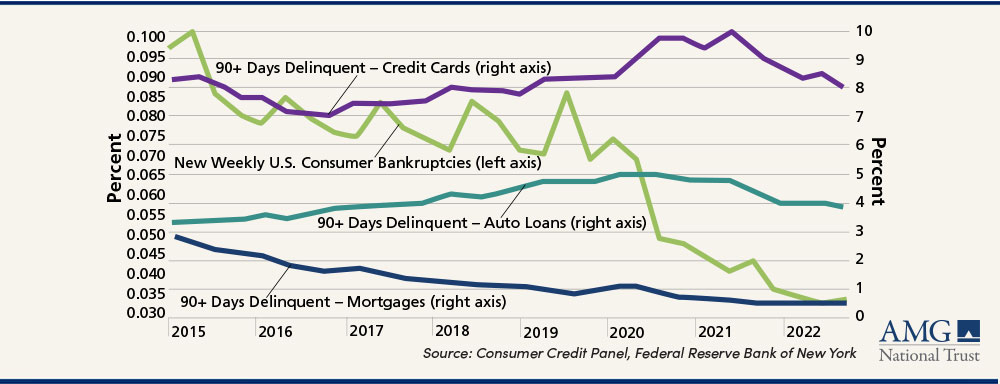

According to AMG’s analysis of key household financial statistics compiled by the Federal Reserve Bank of New York as of late September 2022:

- Weekly filings for consumer bankruptcy protection—a sign of extreme financial distress—are low and declining.

- Serious delinquencies—those overdue by 90 days or longer—on auto loans, mortgages, and credit cards have returned to pre-pandemic levels.

- Notably, credit card debt had experienced an observable uptick in delinquencies during the first year of the pandemic and has since trended down.

U.S. Consumer Bankruptcy Filings & Serious Delinquencies

As interest rates continue to rise, some households will certainly feel a pinch when paying now-higher interest on variable-rate debt. Yet in aggregate, American households are emerging from the last two challenging years with less debt as a proportion of their total household net worth and personal disposable income.

AMG will continue to watch American households’ economic welfare for any early signs of financial distress.